Corporate foreign exchange risk: the complete guide to currency risk management

This article was designed as an in-depth educational resource. Alongside the short and concise formats we also offer (Insight videos, Macroscope, Décryptages), we chose in this article to prioritize density and detailed explanations. The goal is to provide you with a comprehensive understanding of the subject, exploring every nuance.

In today’s globalised economy, shaped by persistent geopolitical tensions and diverging monetary policies between the European Central Bank (ECB) and the US Federal Reserve (Fed), currency volatility is a daily reality. For companies that import, export or operate internationally, being exposed to foreign exchange fluctuations without an appropriate strategy is not risk management, but passive speculation.

A movement of just a few cents in a key currency can instantly wipe out the commercial margin of a carefully negotiated contract. Conversely, a proactive approach to foreign exchange risk management helps secure profitability, stabilise cash flows and provide a significant competitive advantage.

This comprehensive guide covers every stage of foreign exchange risk management, from accurately identifying exposures and implementing a robust governance framework, to building reliable budget assumptions and selecting the most appropriate hedging instruments.

1. Identifying and mapping foreign exchange risk exposures

The first step in effective corporate foreign exchange risk management is to accurately measure and classify the nature of each exposure. Too many organisations take a purely accounting-based approach, overlooking underlying economic risks. In practice, there are three fundamental types of foreign exchange exposure.

A. Transaction exposure

Transaction exposure is the most tangible form of foreign exchange risk, directly affecting both the income statement and operating cash flow. It arises whenever a company commits to a financial transaction, whether a purchase or a sale, denominated in a currency other than its functional currency, which is typically the euro for a French company. This exposure may be internal, such as intercompany transactions, or external, and may be operational or financial in nature.

The life cycle of transaction exposure can be divided into several stages:

- Pre-invoicing exposure, also known as quotation, catalogue or budget exposure: The company issues a quotation, publishes a price list in a foreign currency, or simply knows that it will buy or sell a minimum volume of products in a foreign currency over the coming years, as is common in consumer goods industries. If exchange rates move unfavourably before the contract is signed or before the purchase or sale takes place, expected margins are already reduced, leading to budget variances.

- Order exposure: The contract has been signed, but the invoice has not yet been issued. The commercial commitment is firm, but the expected margin remains exposed to exchange rate movements.

- Invoicing exposure: The receivable or payable has been recognised on the balance sheet. Exchange rate fluctuations will affect the final amount received or paid when settlement takes place.

B. Translation exposure

Translation exposure primarily affects multinational groups and mid sized companies with subsidiaries outside the euro area. At each reporting date, the finance department must consolidate the financial statements, including the balance sheet and income statement, of all entities operating in different currencies.

The assets, liabilities and income statements of subsidiaries denominated in currencies such as US dollars, Japanese yen or British pounds must be translated into the parent company's reporting currency, using either the closing exchange rate or the average annual rate, depending on the accounting rules applied. Although this is primarily an accounting and reporting issue and does not directly affect cash flows, it can significantly influence consolidated leverage ratios, shareholders' equity, and investors' or rating agencies' perception of the group. It may also affect compliance with banking covenants.

C. Economic exposure

Often overlooked because it is difficult to quantify and is frequently not linked to a specific accounting item, economic exposure measures the impact of exchange rate movements on a company's overall business performance, long term value and competitive position. It also reflects the company's ability to compete with businesses whose functional currency has moved more favourably from the customer's perspective.

This loss of competitiveness may result in lower revenue and cannot be hedged in the same way as a future transaction exposure because there is no identifiable underlying transaction. In practical terms, certain future sales or cash flows may simply never materialise because customers choose a local competitor whose currency has depreciated, making its products or services more attractive.

2. Defining the risk management policy and establishing the budget rate

A foreign exchange hedging strategy should never be opportunistic or speculative. It should be formalised in a Foreign Exchange Risk Management Policy approved by senior management and, where appropriate, by shareholders or the audit committee.

At the heart of this policy are several key parameters, including what should be hedged, the target hedge ratio, when and how quickly exposures should be hedged, and the minimum acceptable exchange rate that must be protected. This reference level is commonly referred to as the budget rate.

Different hedging strategies

The policy should define the company's overall approach to foreign exchange risk management:

- The micro hedging approach: A hedge is set up for each individual underlying exposure. This makes it easier to identify each hedging relationship, but day to day management can become complex when dealing with a large number of hedges.

- The macro hedging approach (portfolio based): Exposures in the same currency and with the same maturity are offset against each other through netting. Blocks of exposures may then be hedged using a single hedge, or blocks of hedges may be linked to blocks of underlying exposures.

Different hedging timelines

For these different approaches, the outcome can vary significantly depending on whether the company hedges its exposures when they arise for accounting purposes, at the invoicing stage, as soon as a contract is signed, or even earlier, when preparing the annual budget or a multi year plan.

The earlier a company hedges, the more it protects its actual margins in relation to budgeted margins. If it hedges only at the invoicing stage, it protects its accounting risks, but not its economic risks, its budgeted income statement, or its budgeted cash flow.

It should be noted that the hedge ratio may be progressive. For example, 50% may be hedged during the budgeting process, with the remainder added over the following months so that 100% of invoiced flows are hedged no later than the time they are issued or received, and even more so by the time they are paid. Several methods and rationales exist, to be combined depending on the company’s sensitivity to exchange rate movements, the reliability of its forecasts, and its ability to absorb or pass on exchange differences to customers or suppliers during the year, etc...

How should a budget rate be set and used?

The budget rate is the theoretical exchange rate often used by the finance department and the relevant operational teams, such as purchasing and sales, to prepare their forecasts for sales, purchases and profitability for the coming financial year. It often serves as a reference point until the end of the year.

- If the market exchange rate is more favourable than the budget rate: The company generates a foreign exchange opportunity or a foreign exchange gain.

- If the market exchange rate is less favourable than the budget rate: The company incurs a foreign exchange loss that erodes its industrial or commercial margin.

Several methodologies can be used to determine this rate, each based on a different reference point:

- The year end spot rate: Simple, but arbitrary. It assumes that current market conditions will continue. This is dangerous because it is wrong most of the time.

- Analysts' forecast rate: Using banks' forecasts to anticipate future exchange rate movements is a strategy that is too often used, creating a false sense of security and reducing accountability. It is not recommended because forecasters have a very poor track record. See the Kerius Finance Market Insights on the backtesting of foreign exchange forecasts, which highlights the regular, and sometimes substantial, forecasting errors.

- The market forward rate (Forward Rate): More rational, as it incorporates the interest rate differential between currencies and reflects the rate at which the company can effectively hedge immediately for future maturities. However, without actually implementing a hedging strategy, this method is also often ineffective.

- The weighted historical average: This smooths exchange rate volatility over the previous 12 or 24 months in order to avoid budgeting at a market peak or trough. It becomes ineffective as soon as a market shock occurs.

- The weighted average of existing hedges, or hedges implemented at the time of budgeting: As part of a budgeting process based on a hedging programme that has already begun, the budget rate is determined using the weighted average rate of the hedging instruments already in place, whether forward contracts or options, plus a safety margin to take into account the portion that remains unhedged at the beginning of the programme and the volatility of the currencies. The advantage of this approach is that it faithfully reflects the hedging strategy actually implemented by the company.

3. The treasurer's toolbox: analysis of foreign exchange hedging instruments and speculative products

The choice of foreign exchange hedging instruments or speculative products depends on the objectives of the risk policy, the degree of certainty of future cash flows, the sensitivity of the company's selling prices to exchange rate movements, and the level of flexibility required. These instruments fall into two main categories: firm (commitment) instruments and conditional (optional) instruments. Within the optional instruments, it is important to distinguish between insurance type instruments, based on the net purchase of options, and speculative instruments (Isolated Open Positions for accounting purposes), which are net sellers of options (in terms of amount and/or maturity). We do not recommend the latter for companies seeking to protect their margins, as they can be extremely dangerous.

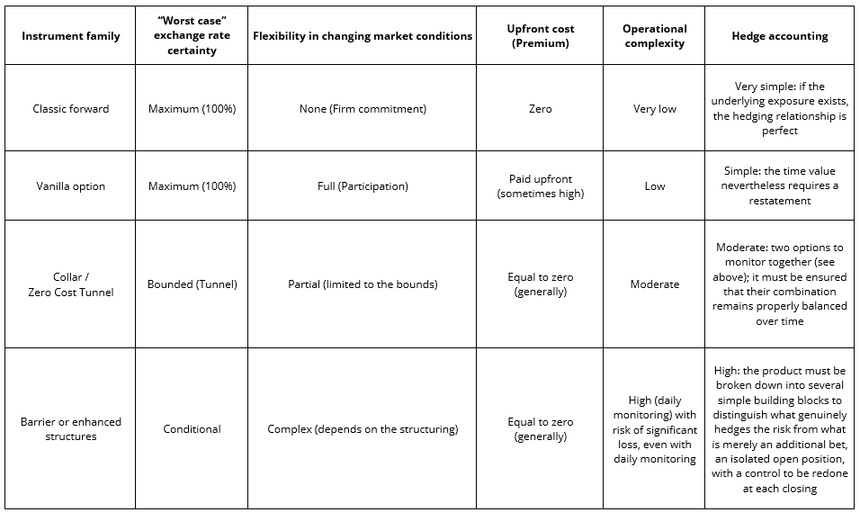

A. Firm instruments (plain vanilla/simple and linear)

1. Spot transaction (Spot)

A Spot transaction consists of exchanging one currency for another at the current market rate, with standard settlement on D+2.

- Use case: Immediate payment of foreign supplier invoices or repatriation of cash flows. It provides no protection against future foreign exchange risk. It is therefore not a hedge in the strict sense of the term. It is used to settle an invoice when no hedging transaction has been put in place beforehand.

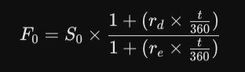

2. Forward

The Forward is the fundamental instrument for foreign exchange risk management. It is a firm commitment to buy or sell a specified amount of currency on a predetermined future date, at an exchange rate fixed today (the forward rate)

The forward rate is not a market forecast. It is calculated mathematically using the interest rate parity formula shown below. Forward points (or swap points) are proportional to the interest rate differential between the two currencies involved in the forward transaction. They may be favourable or unfavourable depending on the interest rate environment.

Where :

- F₀ = Forward exchange rate

- S₀ = Spot exchange rate

- rᵈ = Domestic currency interest rate

- rᵉ = Foreign currency interest rate

- t = Number of days to maturity

Advantage : Absolute certainty. The cost of the hedge is zero at inception (no premium to pay), and the company is protected against adverse currency movements.

Disadvantage: If the market moves significantly in the company's favour, the company remains locked into the agreed forward rate and cannot benefit from the favourable market movement.

Note: The forward hedge maturity date is fixed but can easily be amended (through an extension or early delivery via an FX swap) to align it with the actual payment or collection date.

B. Conditional instruments (vanilla options or plain options)

An option provides complete flexibility. The buyer of an option acquires the right (but not the obligation) to buy (Call) or sell (Put) a currency at a predetermined price (the Strike Price) on a specified date (European style) or at any time during the life of the contract (American style).

In exchange for this asymmetric protection (the option buyer cannot incur losses beyond the premium paid), the buyer must pay the seller a premium (the cost of the option, corresponding to the probability-weighted expected gain that the option may provide, plus the bank's margin) when the strategy is entered into. This premium depends notably on the currency's volatility, the option's maturity and the distance between the strike price and the spot or forward rate, depending on the type of option..

- Unfavourable market scenario: The company exercises its option and remains protected at the Strike price.

- Favourable market scenario: The company lets the option expire (losing only the premium) and executes its transactions directly at the prevailing market rate to maximise its gains.

It is always possible to sell an option before its maturity if it still has value but is no longer useful: for example, if the underlying exposure no longer exists or if the option is replaced by a forward hedge at an advantageous point in time to capture and secure part of the unrealised gain.

C. Structured products: optimising cost while compromising protection

To avoid paying an upfront premium while retaining part of the flexibility offered by options, banks and brokers offer structured products. These consist of a simultaneous combination of purchased and sold options (vanilla or more complex structures).

1. The Collar

A Collar consists of purchasing an option for protection on one side (e.g. buying a Put to hedge a future currency sale) while simultaneously selling another option to fully or partially finance the first one (e.g. selling a Call).

- Result: A "zero-premium" or "reduced-premium" structure under which the company is protected beyond a predetermined floor rate ("worst-case rate") but gives up potential gains beyond a predefined cap ("best-case rate"). At maturity, its effective exchange rate will necessarily remain within this corridor.

2. Participating Forward (non-standard marketing term)

This instrument generally guarantees a minimum protection rate (usually less favourable than a standard forward contract) while allowing the company to participate in favourable market movements for a specified proportion of the exposure (for example, 50% of the hedged amount, depending on the structure).

Be cautious with these so-called "enhanced" products, which may conceal risks arising from embedded sold options, even though this may not be explicitly stated in the product documentation. Currency losses can be significant.

3. Barrier structures (Knock-In / Knock-Out)

These products include activation (the product comes into existence) or deactivation (the product permanently ceases to exist) conditions. If the spot rate reaches a predefined level (the barrier) during the life of the product or at maturity, depending on the structure, the protection is either activated or immediately cancelled, leaving the company exposed to the prevailing market rate or to a less favourable replacement rate. Although these products may initially offer attractive exchange rates, they carry the risk of losing the hedge, potentially at the very moment when protection is most needed. They are generally considered toxic products and are not recognised as accounting hedges. We strongly advise against using them without a thorough prior analysis to verify that the Knock-In/Knock-Out clauses are fully symmetrical with equivalent but opposite clauses on the underlying risk, which is very rarely the case.

4. Accumulator-type structures (marketed under various commercial names): avoid!!!

These speculative structures offer enhanced returns (which are ultimately fairly limited once the often substantial structuring fees charged by banks have been deducted) generated through embedded sold options. They have repeatedly caused significant losses during major currency movements (and in some cases even corporate bankruptcies), whether exchange rates move favourably or unfavourably, due to the risks created by the various embedded sold options. Les The drawbacks of these products are rarely fully understood by CFOs. We strongly advise against using them.

For more information on hedge accounting, read our Insight: Hedge Accounting: optimizing your IFRS reporting (IFRS 9, 13 & 16) without increasing process complexity.

4. Hedge accounting and IFRS 9: the financial impacts

For companies reporting under International Financial Reporting Standards (IFRS), foreign exchange risk management must incorporate the strict requirements of hedge accounting, as set out in IFRS 9.

Without the application of hedge accounting, changes in the fair value (Mark-to-Market) of derivative instruments (forwards, options) must be recognised directly in the income statement at each interim reporting date. This creates significant artificial volatility in net income, completely disconnected from the economic reality of the underlying transactions, and does not protect revenue, operating profit or EBITDA.

To qualify for hedge accounting under IFRS 9, three conditions must be met:

- Formal documentation from inception: The company must formally document the hedging relationship, the risk management objective, the nature of the risk being hedged, and the hedging instrument used.

- A genuine economic relationship: There must be a clear alignment between the characteristics of the hedged item (amount, currency, maturity) and those of the hedging instrument.

- A balanced hedge effectiveness ratio: Hedge effectiveness must meet three specific criteria:

- A hedging relationship: The economic cash flows generated by the hedge must offset those of the hedged item.

- Credit risk must not be the dominant factor: Changes in value resulting from the economic relationship must not be dominated by the effect of the counterparty's credit risk.

- A consistent hedge ratio: The hedge ratio designated for hedge accounting purposes must be the same as the hedge ratio actually used for economic risk management (i.e. no artificial over-hedging to influence reported earnings).

Implementing these strategies requires a thorough understanding of the underlying accounting entries. To learn more about the regulatory aspects, discover our practical guide to optimising your IFRS 9 hedge accounting reporting without adding complexity to your day-to-day processes.

5. Implementing robust foreign exchange risk governance

The failure of foreign exchange strategies sometimes results from the use of tools that are not suited to the company's economic objectives, but not exclusively. Even in such cases, failure most often stems from weaknesses in strategy, organisation and controls (both internal and external), leaving room for opportunistic behaviour and undesirable risk taking. Institutional level governance is based on a strict segregation of duties and the alignment of teams through dedicated committees.

Segregation of operational duties: the Front / Middle / Back Office model

Inspired by bank trading rooms, this organisation is essential to eliminate or rapidly detect operational errors, conflicts of interest and fraud.

1. Front Office (execution)

The treasurer or FX dealer is in direct contact with financial counterparties. Their role is to collect foreign currency exposures from the group's legal entities from another finance department that has measured them (such as Financial Controlling or FP&A), organise competition between banks, and negotiate the best execution rates.

2. Middle Office (control)

Completely independent from the Front Office, the Middle Office verifies that transactions strictly comply with the limits and guidelines defined in the risk policy. It calculates key indicators such as Value at Risk (VaR) - which measures the maximum potential loss of the foreign exchange portfolio over a given time horizon at a specified confidence level (e.g. 95%) - and monitors, in a straightforward manner, hedge ratios and hedge effectiveness against budgeted exposures.

3. Back Office (administration)

The Back Office takes over once the transaction has been executed. It receives confirmations from the banks, reconciles them with the internal dealing tickets, validates settlement instructions, and prepares the accounting entries.

In an SME, it is difficult to have several separate departments. It is therefore the responsibility of the CFO, the shareholders and the Statutory Auditors to ensure that appropriate checks and balances are in place, so that no single individual has the authority to measure exposures, hedge them, manage the back office (security alerts may come from banks requesting margin calls on unusually loss making products), and determine the accounting treatment of hedging transactions without external oversight.

The FX Committee: a strategic decision making body

An FX Committee, or an equivalent body, should meet at regular intervals (monthly or quarterly) and include:

- Shareholders, because foreign exchange risk, when material, falls under the responsibility of shareholders and directors.

- The Chief Financial Officer (CFO)

- The Head of Treasury or Treasurer, where applicable.

- The Purchasing Director (where analysing forecasts for raw material or finished goods purchases denominated in foreign currencies is relevant)

- The Sales Director, where appropriate, to align export pricing policies with hedging strategies (for example, by preventing sales teams from reducing foreign currency selling prices if revenue has already been hedged based on a higher selling price).

The typical agenda of an FX Committee includes reviewing budgets and actual performance to date, analysing variances against the budget rate, reassessing the forecast order book, and approving the use of new instruments in accordance with the strategy validated by the shareholders (most often on an annual basis), or adjusting the hedging programme upwards or downwards. The conclusions of this committee are also useful for the Statutory Auditors when assessing the relevance of the hedging strategy and deciding whether to accept hedge accounting treatment.

6. Methodological checklist to audit your foreign exchange risk management

If you wish to assess your organisation's level of maturity in managing foreign exchange risk, review these 5 key questions (illustrative but not exhaustive):

- Scope of data collection: Do you have a tool (TMS, ERP) or a centralisation process enabling you to consolidate (in real time or with a delay) invoices denominated in non functional currencies from all your exposed subsidiaries?

- Intercompany financing: Do you finance your subsidiaries outside the euro area in your own currency or in theirs? If you finance them in your own currency, do they have the expertise to hedge their risks, manage and account for hedging transactions in order to secure repayments to the parent company?

- Budget modelling: Does your budget rate incorporate swap points (interest rate differentials), is it based on hedging transactions, or does it rely on a simple arbitrary forecast?

- Control of hidden costs: Do you regularly measure the margins applied by your banking counterparties (spreads) against the actual interbank exchange rate at the time of execution? These margins, particularly on structured or enhanced products, can reduce cash flow, but also the effectiveness of hedging transactions and cause them to lose their hedge accounting status.

- Portfolio flexibility: In the event of the cancellation or loss of a major customer order, does your policy and expertise allow you to extend or unwind a hedging contract early without significant penalties (Early Take Up or Extension), or absorb it within the remaining exposures for the year? An extension into another financial year may result in foreign exchange gains or losses being recognised over both financial years and distort financial results and banking covenants.

- Security and compliance: Do your approval processes comply with the four eyes principle or segregation of duties, and with the requirements of European financial regulations?

Conclusion: from a cost centre to a performance driver

Modern foreign exchange risk management has gone far beyond simple accounting hedging. In an unstable macroeconomic environment, it has become a core management discipline. Securing margins through a rigorous hedging policy, mastering risk asymmetry, its consequences and strategic options, and implementing transparent front to back governance are the hallmarks of a resilient finance function.

At Kerius Finance, we leverage our expertise in the foreign exchange markets and our experience in corporate risk management to support SMEs, mid sized companies, large corporations, NGOs and foundations. We design tailored hedging strategies with an insurance based approach, audit your risk management processes, and optimise your operational execution costs.

Choosing to work with independent experts is often a key success factor. In a dedicated article, we explain why independent financial advice has become the leading performance driver for CFOs when dealing with bank trading desks.

Optimise your foreign exchange strategy today

Do you need an independent audit of your foreign exchange exposures or support in structuring your hedging policy?

Our experienced consultants will help you build a robust governance framework, define a tailored hedging policy and strategy aligned with your objectives, and negotiate the best market conditions with your banking partners.

Disclaimer:

Kerius Finance is an independent advisory firm, authorised as a Financial Investment Advisor (CIF) – ORIAS N° 13000716 - Member of ANACOFI-CIF, an association approved by the Autorité des Marchés Financiers (France).

As such, Kerius Finance, which is product and bank-neutral and does not distribute or sell any financial products, only provides personalised recommendations after signing an engagement letter specifying the client's objectives, and carrying out in-depth, personalised analyses.

This document is therefore provided solely for informational and educational purposes. It does not constitute, under any circumstances, a recommendation to enter into any transaction involving the products described herein. The Kerius Finance team remains available to provide further clarification or personalised advice where required.

Please note: banks may offer products that appear identical but contain specific contractual provisions, sometimes subtle, which can significantly affect both the economic outcome and the accounting treatment of the transaction. These products may differ from those presented in this document even when they share the same or a very similar name. Banks may also offer "enhanced" or "dynamic" products, which should be approached with caution and require thorough analysis before implementation.

We recommend in any case that companies which do not have access to an expert treasurer and professional valuation systems seek the support of qualified, regulated advisors to carry out the appropriate analyses, select the right strategy without conflicts of interest, and then negotiate it as effectively as possible (legal terms and pricing) with their usual banking partners. It is also often useful to monitor the strategy over time to ensure that any developments affecting the debt do not require adjustments to the hedging strategy.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.