What Future for the US Dollar?

What Future for the US Dollar?

Donald Trump is increasing tariffs on numerous countries. He seems to aim at correcting the US trade deficit, attracting industries back to American soil, and generating massive tax revenues to fund a significant reduction in income tax. However, according to many economists, these objectives are difficult to reconcile and may even be mutually incompatible.

The logic of imposing a balanced trade in industrial goods with every country is considered unrealistic by many economists, since countries that export industrial goods also import a large amount of services, particularly digital services.

Current analyses suggest that even with heavy import taxation, these strategies will neither cover the deficit ($1.2 trillion per year), nor effectively revive American industry, nor replace income tax. Imports and exports are both likely to decline.

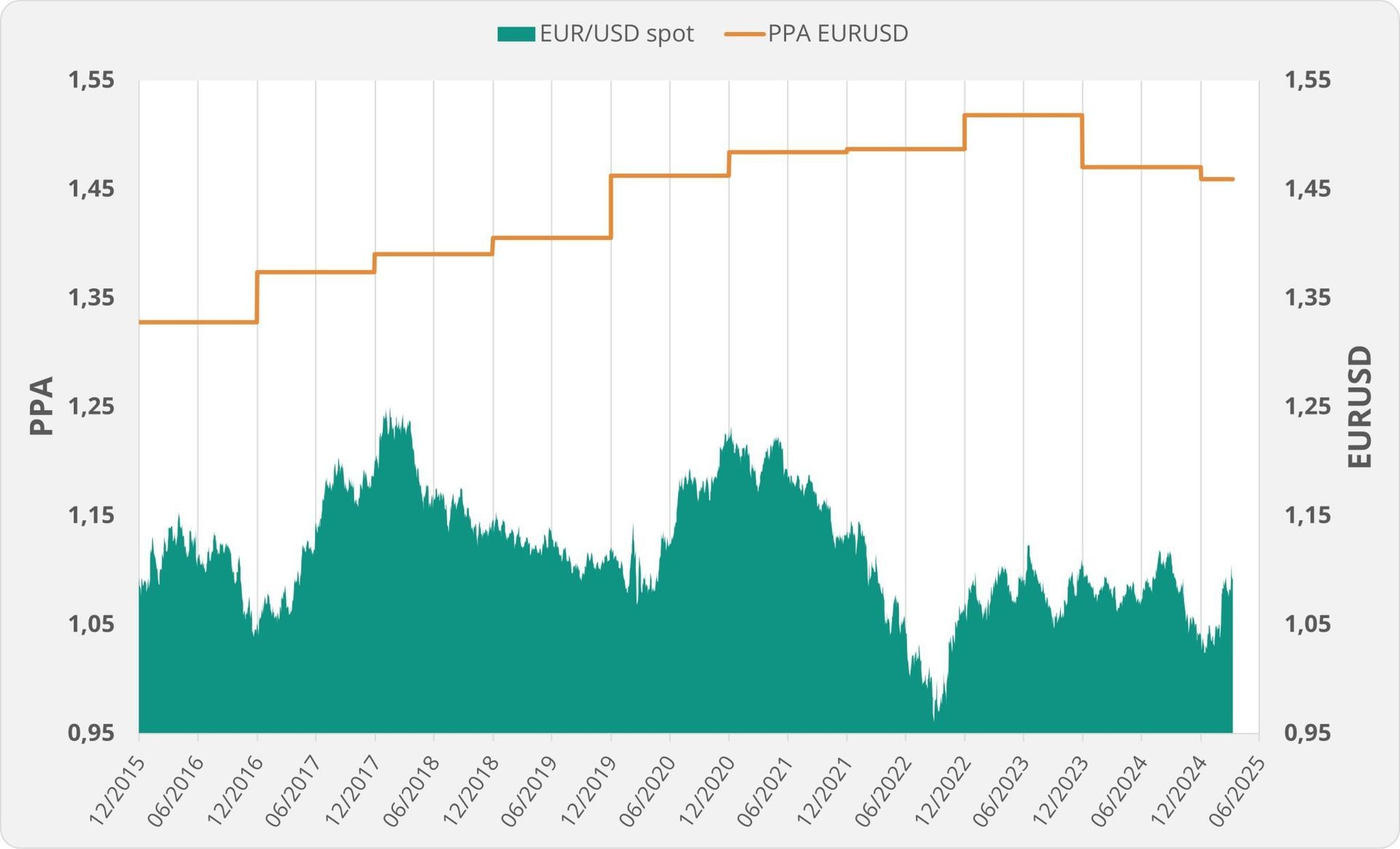

Another potential strategy seems to be emerging: forcing foreign countries to revalue their currencies against the dollar through trade pressure, in order to favor US exports. The euro, currently and for a long time, has been significantly undervalued relative to its Purchasing Power Parity (PPP) with the dollar (currently ~1.12 spot vs. PPP at ~1.45), as shown in the graph below, suggesting that the goal could be to restore this balance.

However, weakening the dollar raises import costs, thereby importing inflation. At the same time, it may reduce the dollar’s dominant position, which is a geopolitical advantage (global demand allows the US to borrow without limits).

The dual objective of weakening the dollar while retaining its status as the world’s reserve currency is risky, unless one assumes the US can force its “clients” to continue buying American debt to maintain monetary hegemony without bearing the burden of a strong dollar.

This is uncertain, however, because aggressive policies are already undermining international confidence in the US and its debt. Investing in US dollar-denominated bonds is perceived as riskier in recent days, and US debt financing rates are rising (~4.40% for 10-year bonds). Currency hedges used to protect bond portfolios against a falling dollar will mechanically weaken the currency, intensifying the feared effect.

In parallel, the Swiss franc and gold (see my previous post), and to a lesser extent the euro, have been serving as safe-haven assets in recent weeks.

Conclusion: The US trade strategy could lead to a devaluation of the dollar, but at the cost of losing monetary hegemony and facing difficulties financing the deficit. This may limit their maneuvering room in the trade war and create numerous market disruptions.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.