Market Letter - September 2025

FOREIGN EXCHANGE MARKET: a summer of high tension

The summer has been particularly eventful on the foreign exchange market.

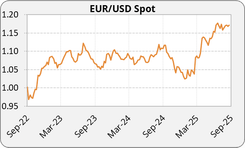

July: The dollar strengthened sharply despite frictions between Donald Trump and Jerome Powell, supported by the new tariffs on BRICS countries and the July 27 agreement with the European Union, which boosted trade. The Fed’s decision to keep rates at 4.25%–4.50% also lent support. EURUSD hit a low of 1.14 on July 30.

Late August: The trend reversed. Jerome Powell’s dovish tone at Jackson Hole (August 22), combined with Donald Trump’s shock announcement to dismiss Fed Governor Lisa Cook, reignited doubts over the central bank’s independence and weakened the dollar. EURUSD rebounded to 1.1728, its highest since late July.

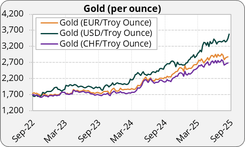

As summer draws to a close, U.S. uncertainty is rattling markets. Early September nonfarm payrolls came in well below expectations, weakening the dollar. Investors are flocking to gold, which has surged to a new record of USD 3,650 per ounce.

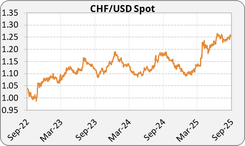

The euro initially fell on French political concerns but quickly rebounded after the appointment of Sébastien Lecornu as the new prime minister, reassuring markets. The euro climbed back to 1.1743 USD and 0.9346 CHF.

Other Currencies:

- The AUD declined following the RBA’s rate cut in July.

- The GBP gained against the euro, supported by the Bank of England’s narrowly split decision to cut its policy rate.

- The CHF strengthened during periods of political turbulence in both the USA and Europe.

- The yen continued to depreciate, with EURJPY reaching 173.

Crypto: After hitting a record high of USD 124,000 in mid-July, bitcoin pulled back sharply, dropping to USD 115,000 and then USD 109,000 by late August. The decline reflects political and monetary uncertainty in the United States, despite occasional support from the prospect of partial integration into certain US retirement savings plans.

INTEREST RATES: The Fed signals a turning point

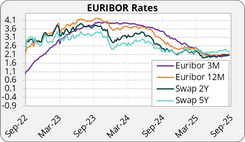

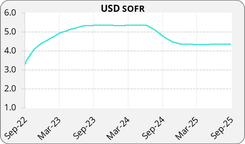

United States: The Fed kept rates at 4.25%–4.50% in July, with Powell signaling a highly probable rate cut in September (over 90% odds). The labor market weakened with only 73,000 jobs created in July with sharp downward revisions for May and June, while inflation (PPI and CPI) accelerated in July, complicating the short-term outlook. Yields stood at 4.30% for the 10-year, 4.94% for the 30-year, and 3.71% for the 2-year, reflecting expectations of an imminent cut. Softer inflation data in August suggested easing price pressures, encouraging the Fed to consider a 25 bps reduction and even leaving room for a 50 bps move. However, the September 11 CPI release, showing inflation rising from 2.7% to 2.9%, complicated the picture despite Powell’s comments on the need to adapt the Fed’s strategy.

Europe: Swap rates remained relatively stable, but French debt came under pressure. The 10-year OAT–Bund spread widened to 77 bps, exacerbated by Prime Minister François Bayrou’s announcement of a confidence vote. France is now borrowing at rates close to or even above those of Italy and Greece. The 5-year swap rate stands at 2.26%, while the 10-year swap rate is at 2.62%.

Other regions:

- Australia: The Reserve Bank cut its policy rate to 3.6%

- United Kingdom: The BoE lowered its rate to 4%, a decision narrowly passed (5 votes to 4).

- Japan: The 10-year yield climbed above 1.62%, its highest since 2008, while the 30-year exceeded 3.20%. Comments from Kazuo Ueda on sustained wage growth reinforced expectations of further monetary tightening by the BoJ. Developments in Japan could act as a catalyst for heightened volatility in the months ahead.

COMMODITIES: Gold extends rally, oil under pressure

Gold: The precious metal regained its safe-haven status. Amid political and monetary tensions, it broke above USD 3,650 per ounce and has held around that level as summer ends.

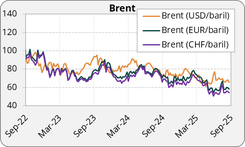

Oil: Brent crude remained stable around USD 65–66 per barrel. Talks between Donald Trump and Vladimir Putin, followed by discussions with Volodymyr Zelensky, raised hopes of de-escalation in Ukraine and a potential easing of sanctions against Moscow. This temporarily weighed on prices.

Industrial Metals: Volatility remained high throughout the summer.

- Aluminum and palladium advanced, supported by expectations of Fed rate cuts and a weaker dollar.

- In contrast, iron ore fell to around CNY 762 per ton, a seven-week low, pressured by China’s property crisis and rising steel inventories.

- Frictions between Washington and New Delhi (U.S. tariffs on Indian exports and threats of sanctions over Russian energy) further amplified volatility.

TARIFFS: Back-to-school update

Current Framework :

A “base” tariff of 10% on nearly all imports, complemented by country-specific “reciprocal tariffs,” plus a special 25% duty on automobiles (measures announced through presidential executive orders in the spring).

China : Extremely high surcharges, with swings between 84–125% on the U.S. side and retaliatory measures from China. The issue remains unresolved and is the main source of tension.

Already negociated :

Japan : Agreement announced in late July, with tariffs reduced to 15% on most goods (including autos) in exchange for a large U.S. investment package (~USD 550 bn). Implementation is still being fine-tuned technically.

European Union : Framework agreement reached in late July targeting a 15% tariff (instead of the 30% initially planned) in exchange for European commitments on investment and purchases (~USD 600 bn).

Still to negociate / Areas of uncertainty

South Korea: Political announcement of a 15% tariff, but no formal agreement yet. Key sticking points remain in agriculture, defense, and investment funds.

Canada / Mexico: Canada remains subject to a 35% tariff (outside USMCA goods) and 25% on automobiles; talks are ongoing for targeted exemptions. Mexico is seeking specific adjustments for the auto sector.

India: No agreement reached; Washington has raised tariffs, and rhetoric remains tense. New Delhi is considering or has already filed WTO complaints.

China: Tariff standoff and ongoing WTO disputes, with no structural truce in sight.

Legal dimension : risk of unvalidation

Key decision: A federal appeals court ruled that most “reciprocal” tariffs imposed under IEEPA are unlawful, arguing that authority lies with Congress.

Next steps: The administration has requested expedited Supreme Court review, with a final ruling expected in 2026. Meanwhile, the White House is considering shifting some measures to alternative legal grounds.

Potential consequences if struck down: Reimbursement of tariffs already collected, renegotiation of bilateral political agreements, and a pivot toward legally stronger and more targeted measures.

This newsletter was written on the 12/09/2025.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.