Market Letter - May 2026

FX : the euro stabilises (temporarily ?) despite the war in the Middle East

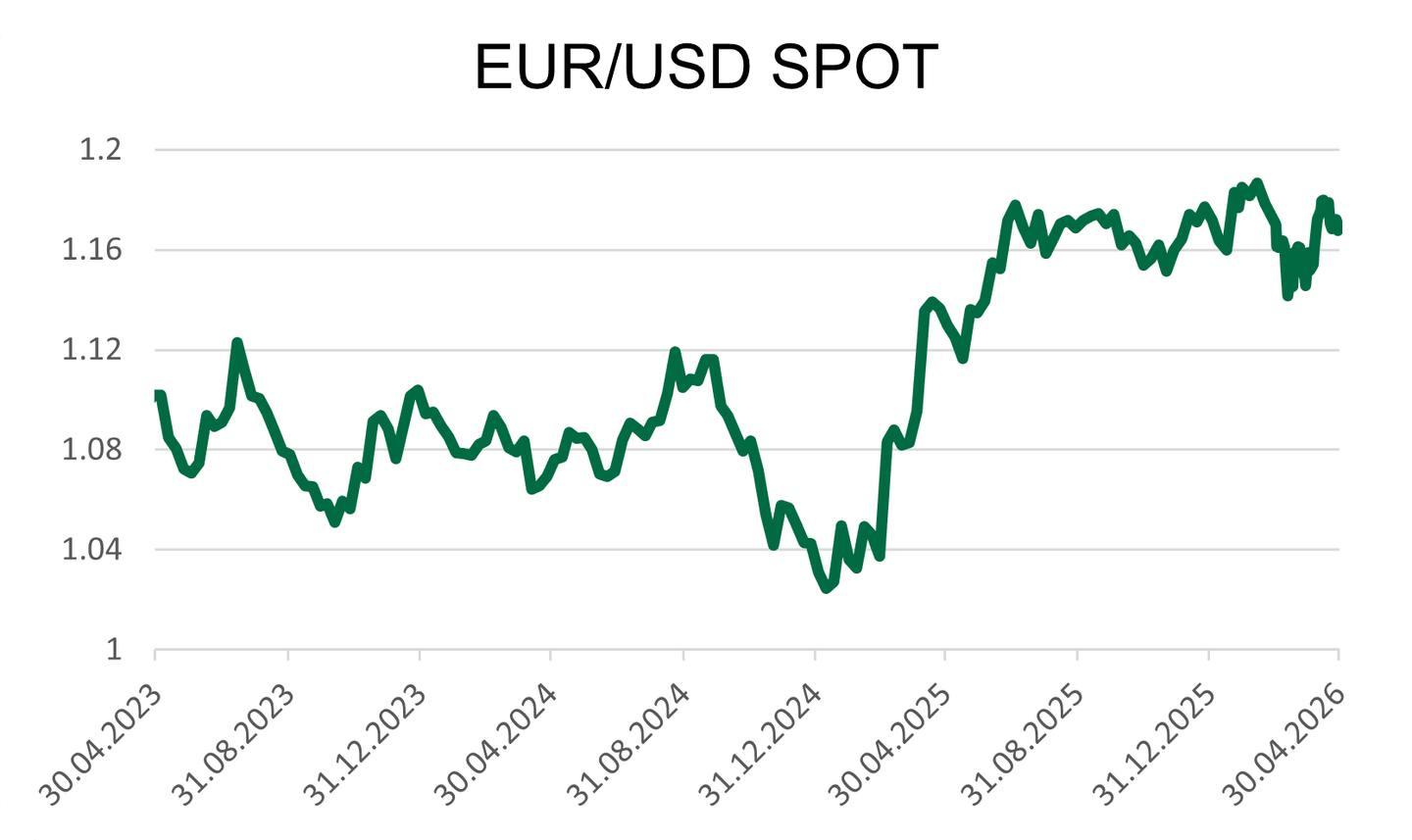

EURUSD: after a March disrupted by the energy shock linked to the war in the Middle East, EURUSD recovered in April and was trading around 1.17 at month-end. The dollar remains supported by its safe-haven role when geopolitical tensions rise, but also by US rates that remain high following the Fed meeting. Conversely, the euro benefited from a slight easing of the stress seen in March. However, the euro area remains directly exposed to higher energy prices, and every upward move in oil continues to weigh on the euro against the dollar.

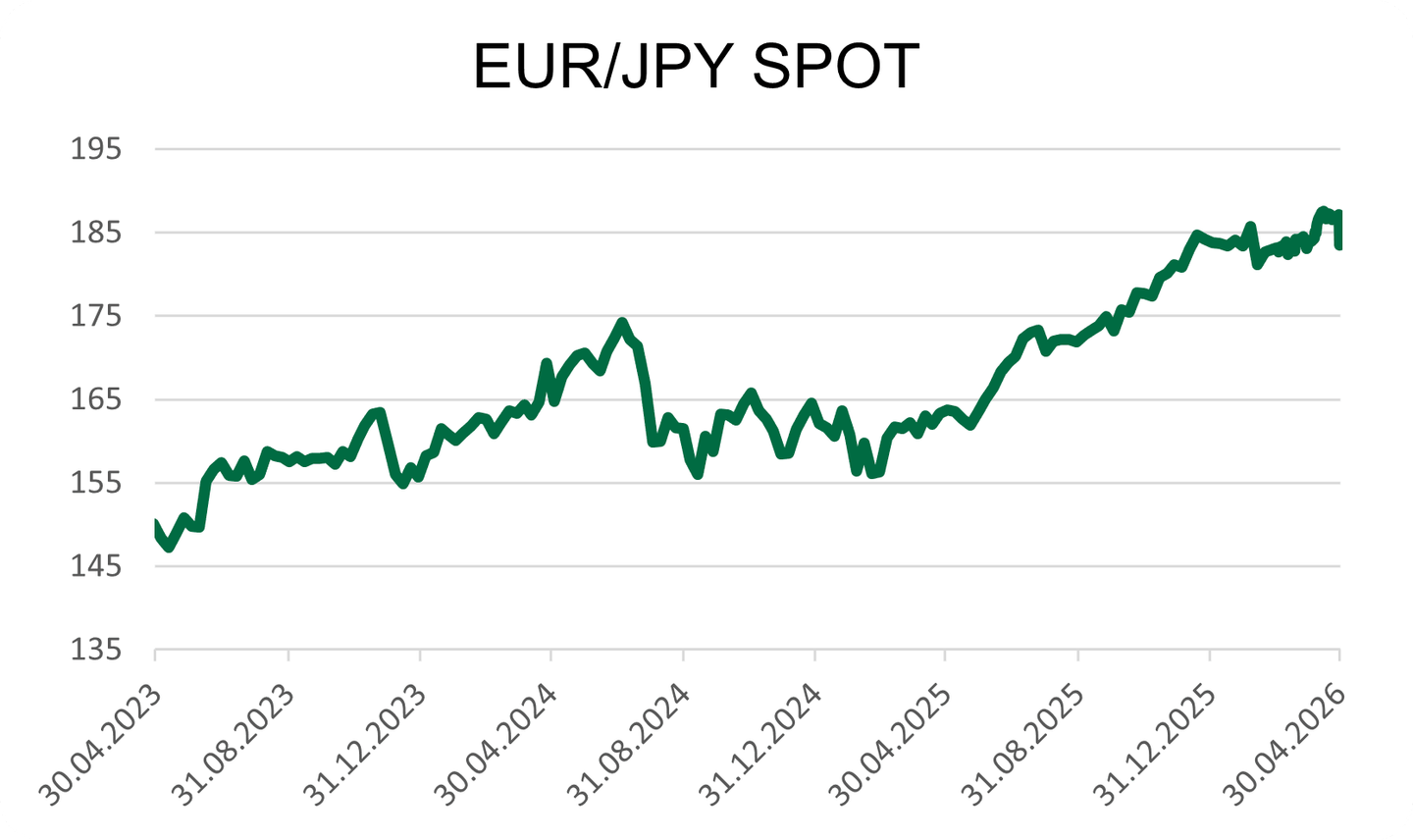

EURJPY: EURJPY experienced a sharp move at the end of the month, after trading at historically high levels near 187. The yen rebounded strongly on Thursday, gaining nearly 3% against major currencies, following several warnings from Japanese authorities about a possible intervention to support the currency.

Japan remains penalised by its dependence on energy imports, while oil prices remain elevated. However, the move shows that Tokyo is not willing to let the yen depreciate without limits. In the short term, EURJPY should therefore remain highly sensitive to intervention signals from Japanese authorities, as well as to oil price developments and expectations of further rate hikes by the Bank of Japan.

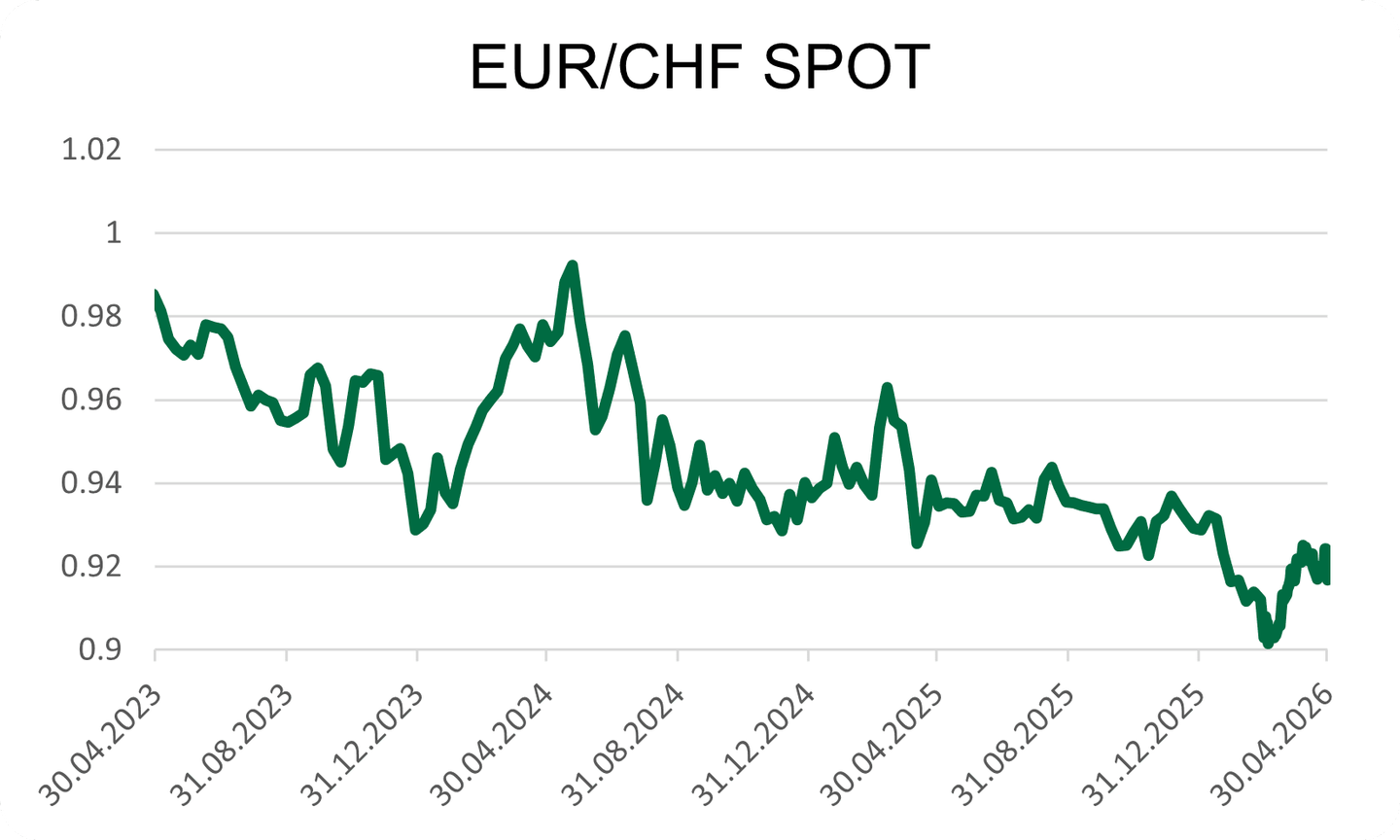

EURCHF: EURCHF recovered to around 0.92, after the lows reached during the March shock. The Swiss franc remains in demand when geopolitical tensions rise, but the pair regained some ground in April as markets partially stabilised. The move remains fragile: if Middle East risks rise again, the franc could strengthen quickly. Conversely, a clearer easing in energy markets or maritime traffic could allow EURCHF to remain above its recent lows. The SNB remains attentive to the level of the franc, as an overly strong currency would weigh on Swiss inflation and exporters.

EURGBP: EURGBP remains close to 0.866, without a clear direction over the month. Sterling held up better than the euro during March’s energy shock, but the gap narrowed in April as markets partially stabilised. The pair remains driven by rate differentials between the UK and the euro area, but also by both economies’ sensitivity to higher energy prices. In the short term, as with the major currencies, EURGBP should react to oil price developments and to the next signals from the Bank of England and the ECB regarding their rate paths.

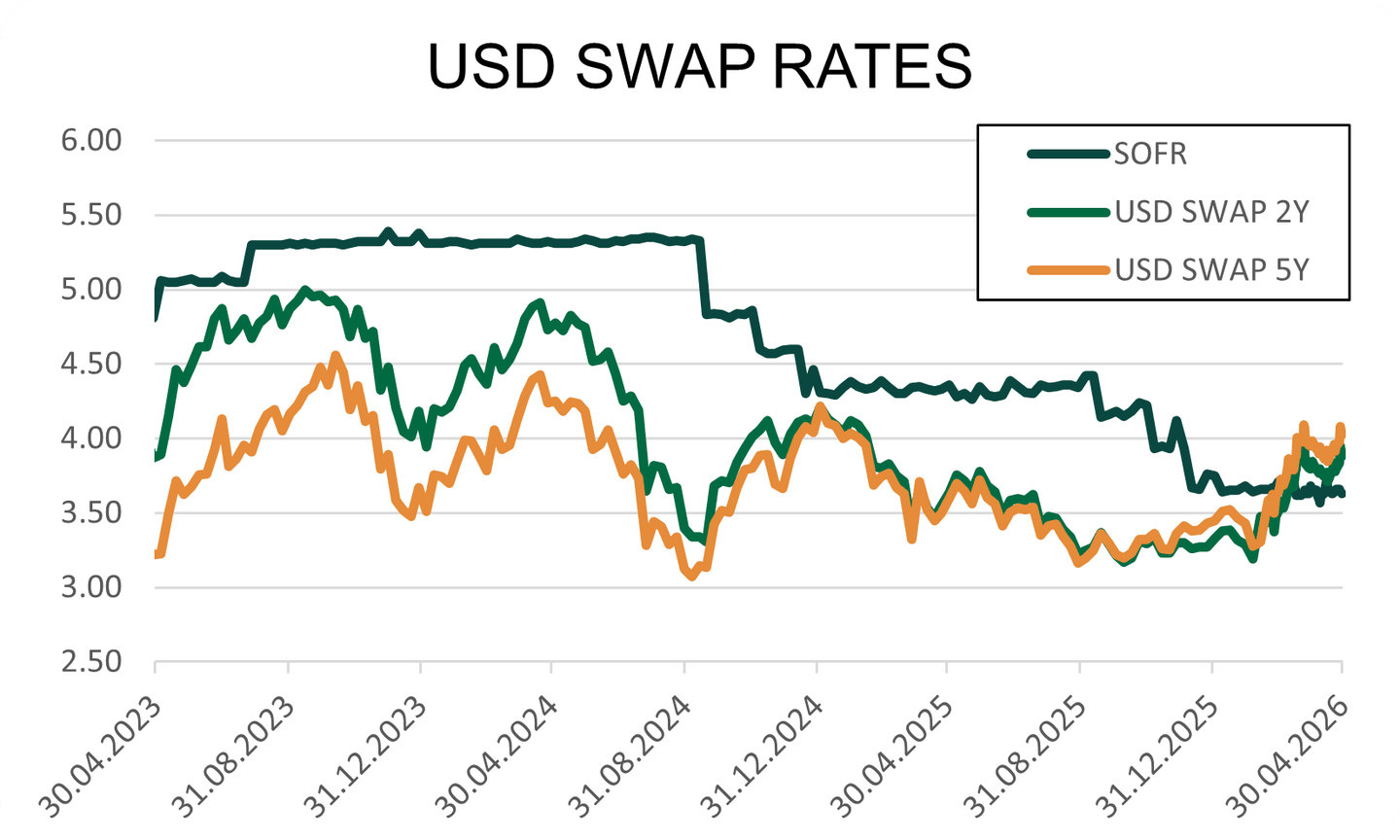

Interest rates: rising inflation complicates central banks’ calendars

United States: US rates remained elevated in April. The USD 5-year rate stands above 4%, while the 10-year Treasury yield is trading around 4.40%. The Fed kept rates unchanged in the 3.50%–3.75% range, as expected. In its statement, it noted that economic activity continues to expand at a solid pace, that job gains remain weak on average, that unemployment has changed little in recent months, and that inflation remains elevated, notably due to the recent rise in energy prices.

During his press conference, Jerome Powell said that inflation had recently increased and that headline PCE inflation was estimated at 3.5% year-on-year in March, driven by the sharp rise in oil prices linked to the conflict in the Middle East.

The vote was more divided than usual, with one member in favour of a 25 bp cut and three others opposing the inclusion of a signal pointing to a future cut in the statement.

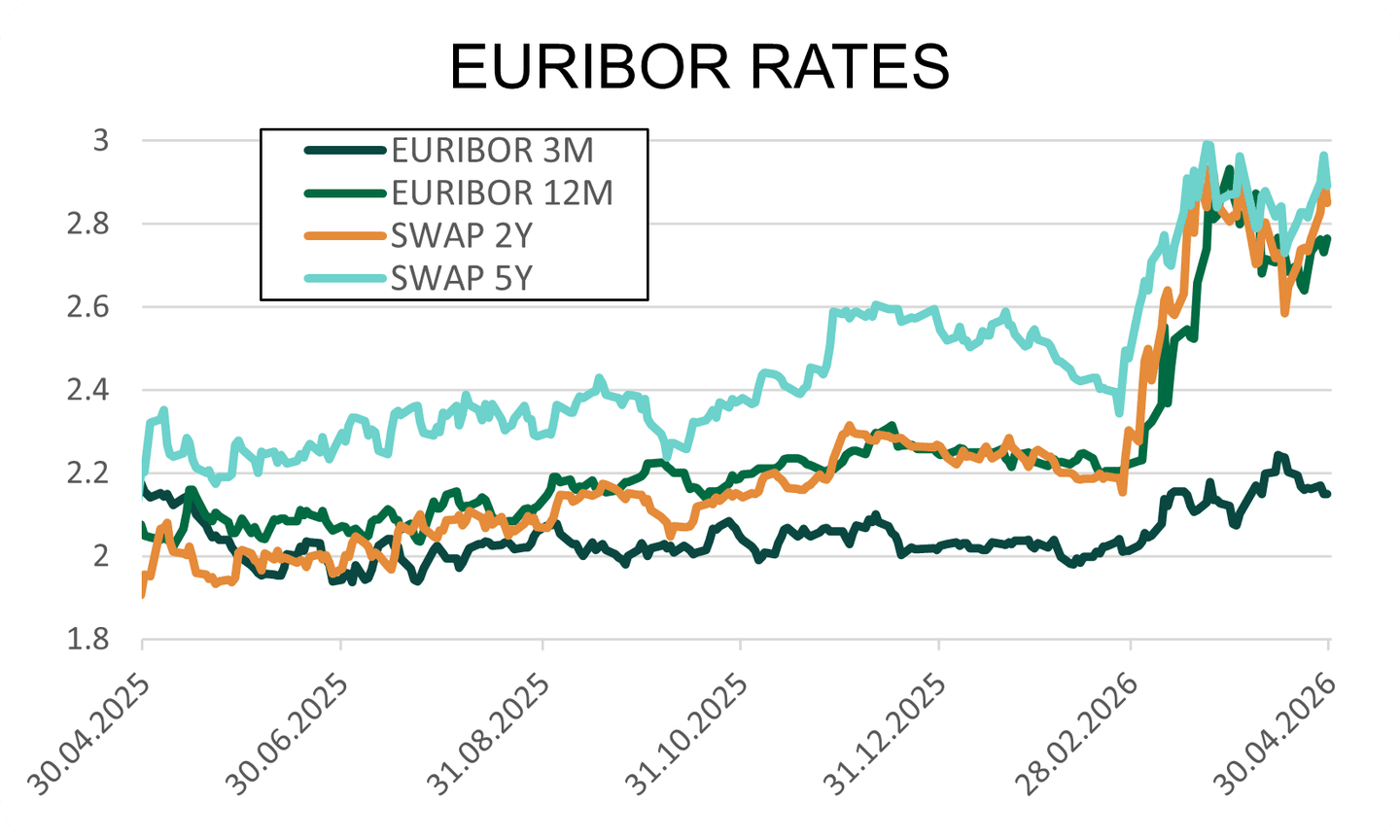

Euro area: European rates remained at very high levels in April, with the EUR 2-year swap rate around 2.85% and the EUR 5-year swap rate around 2.90%. Although a rate hike was discussed, the ECB decided to wait and leave its three key interest rates unchanged, as expected, with the deposit rate held at 2.00%, the refinancing rate at 2.15%, and the marginal lending rate at 2.40%. In its statement, the ECB indicated that upside risks to inflation and downside risks to growth had both increased, mainly due to the energy shock linked to the conflict in the Middle East.

Christine Lagarde also reiterated that the ECB would remain data-dependent and decide meeting by meeting. A 25 bp hike at the June meeting is now priced by the market with a probability of more than 99%.

Japan: the Bank of Japan kept its policy rate unchanged at 0.75%, but the 6–3 vote shows that the internal debate is shifting. Three members already wanted to raise the rate to 1.00%, reflecting stronger concern over inflation risks. The BoJ also raised its inflation forecasts and lowered its growth forecasts, a sign that higher energy prices are making its decision much more difficult: they push prices higher while weighing on activity.

During his press conference, Kazuo Ueda explained that the central bank preferred to wait and assess the effects of the conflict in the Middle East, but that it could raise rates if inflation risks increase and if the economic slowdown remains limited. The market therefore sees Japan’s rate path as still tilted upward, but with the timing dependent on oil prices and their impact on Japanese households and businesses.

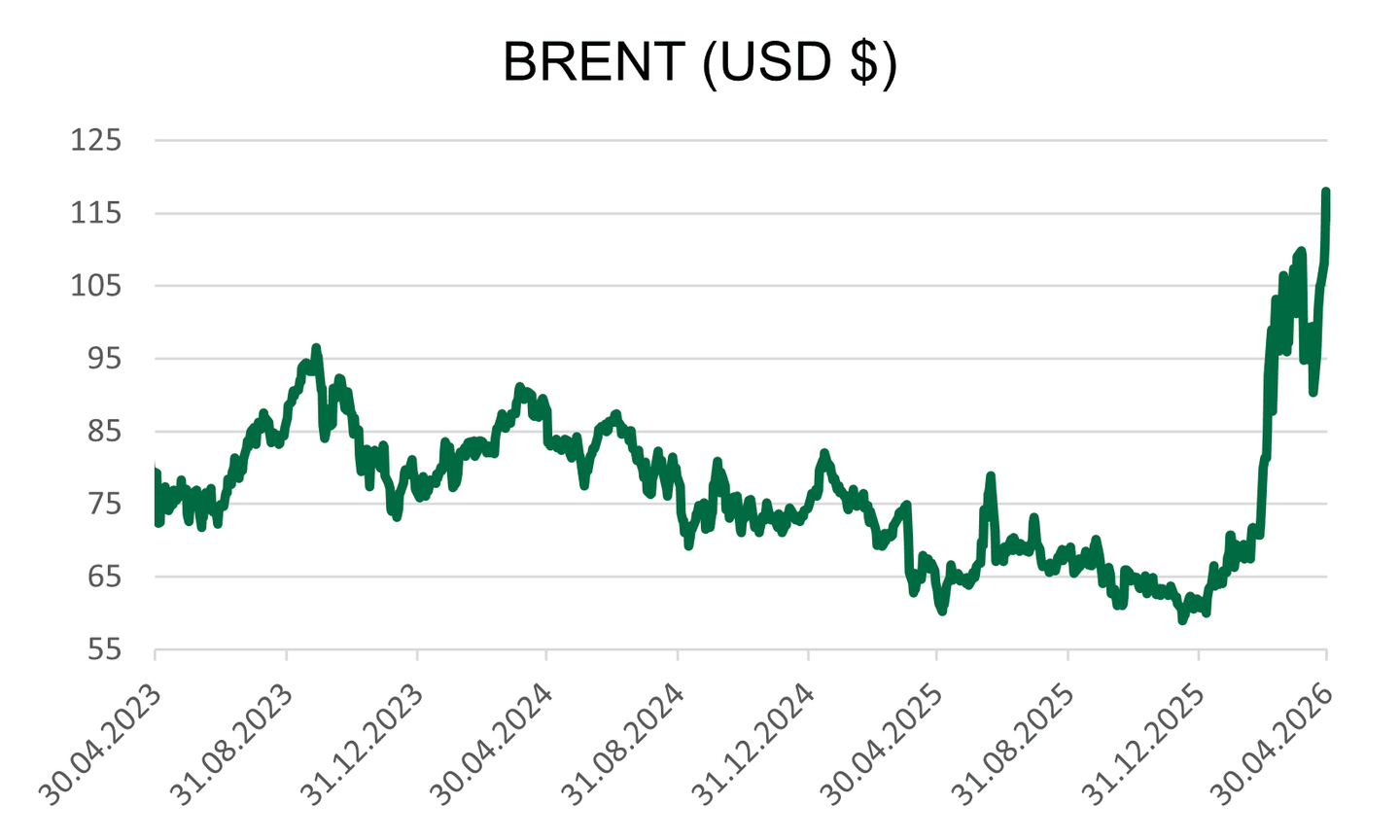

Commodities: the energy shock spreads into industrial costs

Oil: oil remains the central focus of the month. Brent is now trading around $111/barrel, while WTI is around $108/barrel, supported by the absence of an agreement between the United States and Iran and by persistent disruptions around the Strait of Hormuz. The market is now pricing in a concrete risk of physical supply shortages, in a context where oil flows from the Gulf remain heavily disrupted.

The announcement that the United Arab Emirates is withdrawing from OPEC and OPEC+ adds another layer of uncertainty. In the short term, this decision is not enough to push prices lower, as geopolitical risk and supply tensions remain dominant. However, it weakens the cartel’s ability to coordinate production in the coming months, at a time when the market precisely needs more visibility.

The market appears less panicked than at the start of the conflict, but it is now pricing in a structurally higher oil price. As long as the Strait of Hormuz does not clearly reopen and diplomatic talks remain blocked, prices should remain highly sensitive to every political statement, every attack, and maritime traffic data.

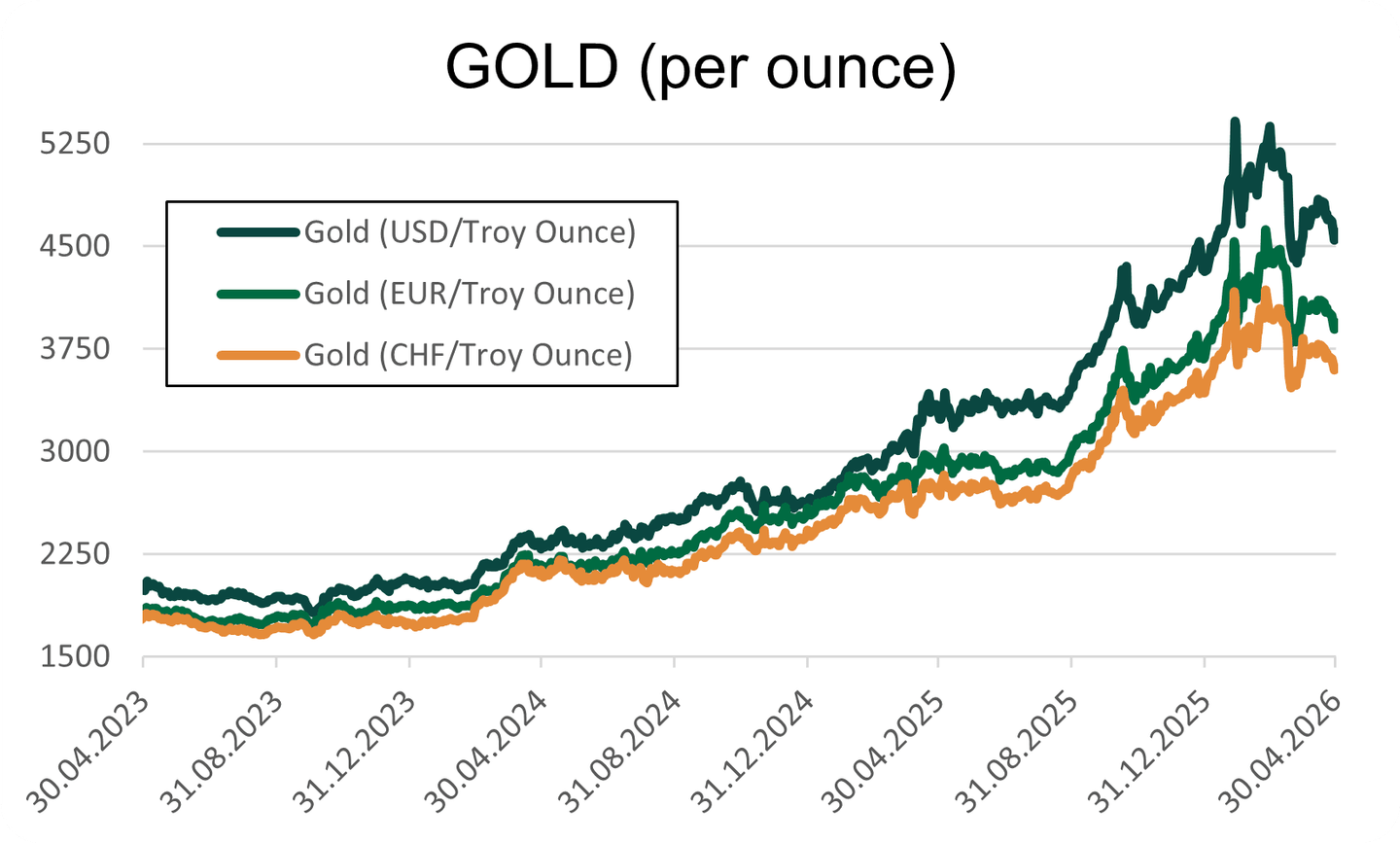

Gold: gold is trading around $4,600/oz, down over the month. Despite the war in the Middle East, precious metals remain penalised by the stronger dollar and by rates that remain high after the Fed meeting. As long as the market moves away from the scenario of rapid rate cuts, gold loses part of its appeal compared with interest-bearing assets.

Silver: silver is trading around $73/oz. The metal remains more volatile than gold because of its strong exposure to industrial demand. As with gold, higher rates are currently limiting its upside potential.

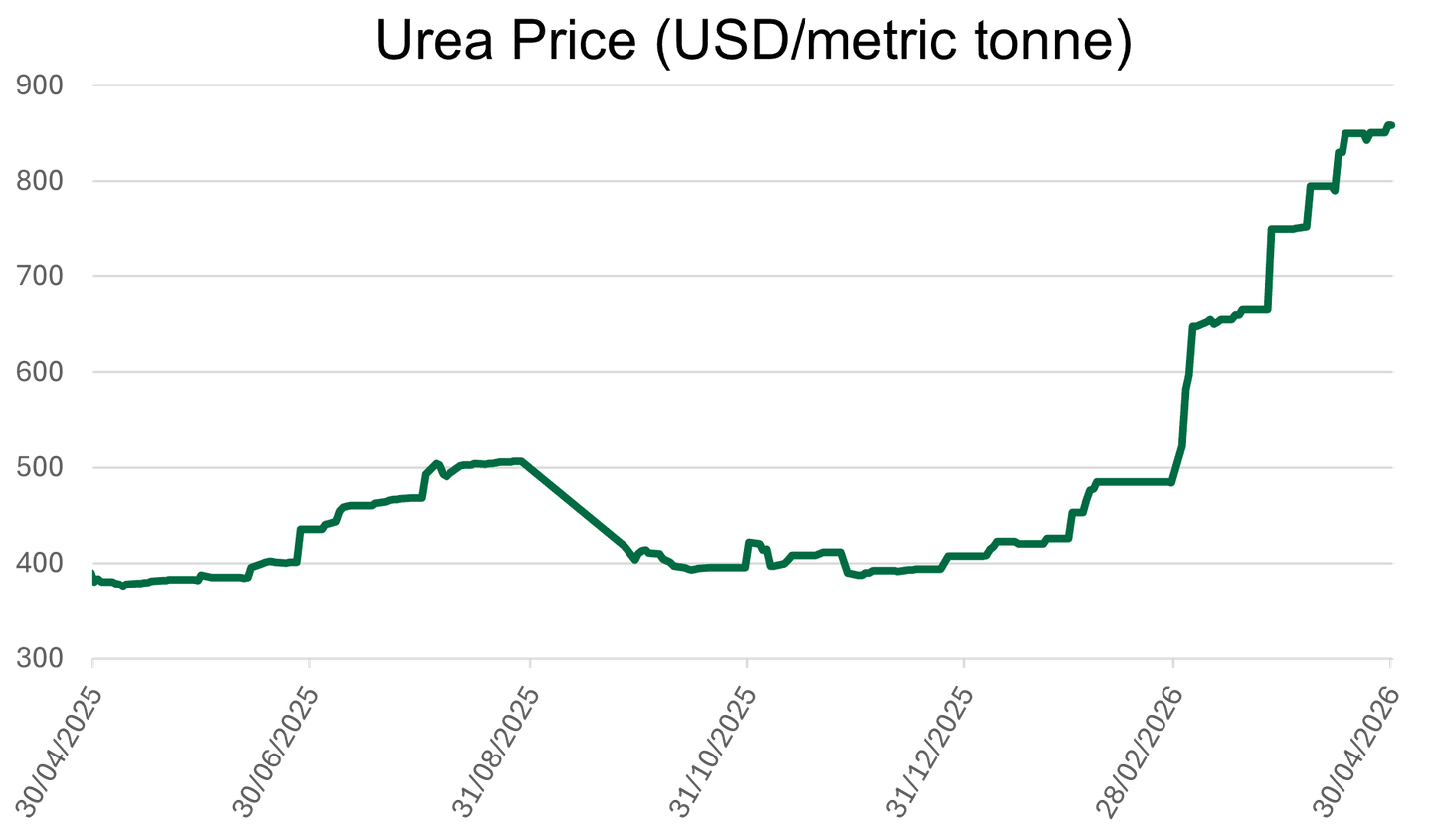

Fertilisers: the shock is no longer limited to oil. Fertilisers are once again becoming a major pressure point, as their production depends heavily on natural gas, particularly for urea. The FOB Middle East benchmark is trading around $850/metric tonne at the end of April. The World Bank now estimates that fertiliser prices could rise by 31% in 2026, driven by an increase of around 60% in urea prices. It also notes that fertiliser affordability for farmers could fall back to its weakest level since 2022.

Gas is more expensive, the Middle East remains an important region for some supply chains, and maritime transport has become more complicated. For companies exposed to agrifood, agriculture, or packaging, the risk is therefore a delayed impact: higher oil prices are visible immediately, while higher fertiliser prices can feed more slowly into agricultural costs and then into food prices.

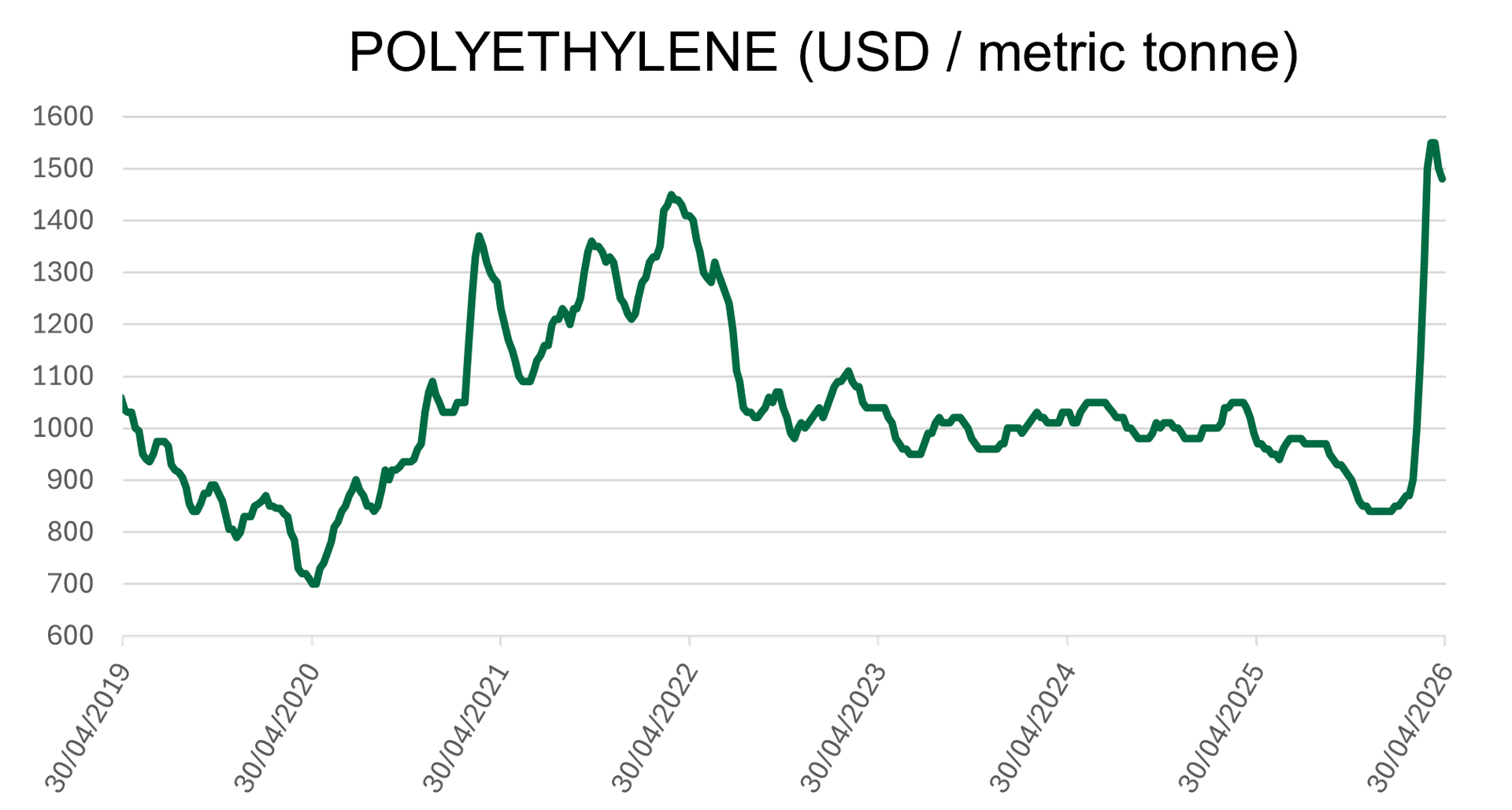

Polyester / PET / petrochemicals: plastics derived from oil are also affected by higher costs. In Europe, polyethylene prices have risen sharply since the start of the conflict in the Middle East, with spot prices doubling on some references since late February, according to ICIS. As an indication, some European PE / HDPE prices are now around €2,000 to €2,500/tonne, depending on grades and markets.

This move directly affects downstream sectors: packaging, textiles, consumer goods, hygiene, and distribution. The shock is therefore not only passing through crude oil, but also through the chemical raw materials used in industrial supply chains.

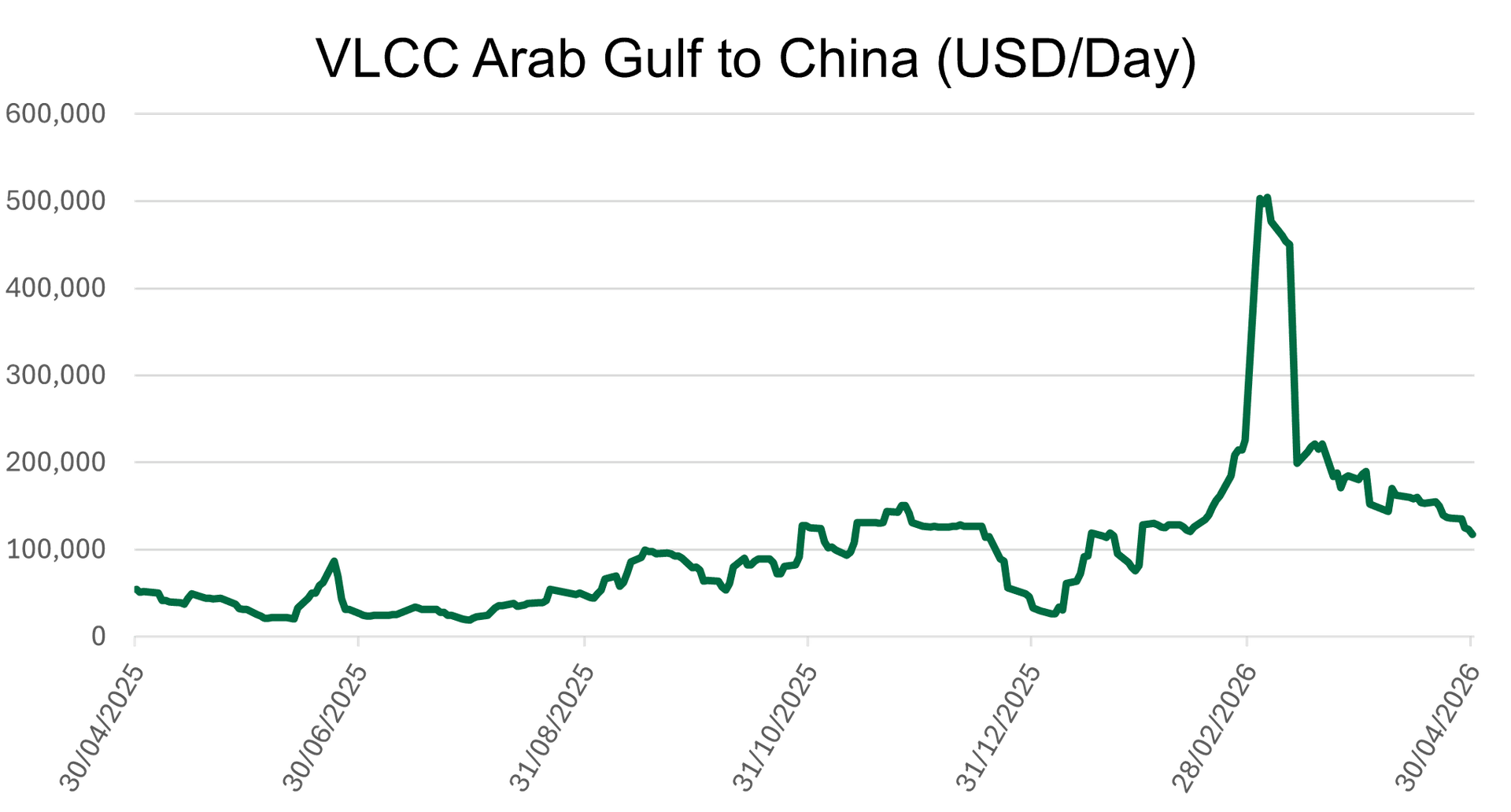

Maritime freight / VLCC: maritime transport has become a cost to watch in its own right. Tensions around the Strait of Hormuz have caused significant volatility for large tankers, with sharp spikes on some spot routes. To smooth out these movements, the 12-month charter rate for a 300,000 DWT VLCC stands at around $105,250/day at the end of April, compared with $99,000/day the previous week.

On the main VLCC route between the Middle East Gulf and China, spot earnings equivalent to time charter rates reached peaks of more than $500,000/day in late February / early March 2026, before falling back towards $117,000/day. The logistical stress is not limited to the price of a barrel: it is also spreading into transport, insurance, and corporate supply costs.

This market report was prepared on 05/01/2026.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.