Market Letter - March 2026

Currencies : Washington sets the pace, the dollar strengthens

EURUSD: after moving above 1.20 at the end of January, the pair corrected through February and settled back around 1.18. Price action was driven by decisions coming out of Washington: the Supreme Court struck down the “global” tariffs, the White House then announced a replacement framework (a temporary 10% tariff with the stated goal of moving to 15%), and the release of the Fed minutes confirmed the Fed is not in a hurry to change rates. This weekend, the jump in Middle East tensions added another leg of USD demand, with Europe more exposed through energy prices, and EURUSD slipped back toward 1.17 at the start of the week.

EURJPY: EURJPY traded in a high range throughout the month, with the yen very data-dependent. In mid-February, softer-than-expected US figures briefly supported the yen. Late in the month, the move became more pronounced: EURJPY climbed back above 184 after a report said Japan’s Prime Minister had expressed reservations to the BoJ about further rate hikes, and after BoJ board appointments were seen as less supportive of a rapid tightening pace. At the same time, USDJPY moved back toward 156, suggesting the move was primarily yen-driven.

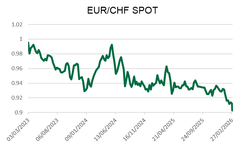

EURCHF: The Swiss franc stayed firm throughout February and continues to be used as a safe-haven, keeping the pair near multi-year lows. EURCHF had already slipped toward 0.91 during the second half of February, and the weekend escalation in the Middle East triggered another drop: the euro touched 0.9020 CHF, its lowest level since 2015, before stabilising slightly above. Switzerland’s backdrop (low inflation and a 0% SNB policy rate) continues to underpin CHF demand, and EUR rebounds versus CHF have remained short-lived.

EURGBP: Moves were more moderate in February. Sterling was relatively firm in the first half of the month, helped by lower UK inflation and a market still focused on the BoE’s policy calendar. The pair ended the month around 0.87, with no lasting impulse.

Interest rates : Widespread pause, the timing of rate cuts under debate

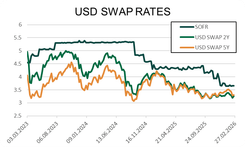

United States: In February, the Fed kept rates unchanged (3.50–3.75) and the market adjusted the expected timing of the next cuts as data were released. January CPI came in less inflationary (0.2% m/m; 2.4% y/y), which pushed rate-cut expectations lower mid-month. The Fed minutes reiterated the Committee wants more confirmation before considering another cut, limiting the overall move. Ultimately, USD swap rates finished the month lower than at the start (the 5-year USD swap fell from 3.85 at the beginning of the month to 3.60 this week), with markets remaining highly reactive to inflation data and Fed commentary. On 30 January, Donald Trump announced the nomination of Kevin Warsh as Fed Chair; if confirmed by the Senate, he would succeed Jerome Powell at the end of Powell’s term, which runs until 15 May 2026. Warsh has recently criticized a Fed viewed as “too slow” and is seen as supportive of at least two 25 bp cuts in 2026. The next FOMC meeting in mid-March is widely expected to deliver no change, with markets pricing roughly a 95–99% probability of a hold. At this stage, the first credible window for a cut looks more like the summer, provided upcoming inflation prints confirm the trend.

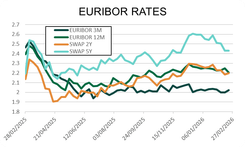

Euro area: In February, the ECB maintained the status quo (deposit rate at 2.00%) and the message was unchanged: no rush to move as long as inflation does not reaccelerate. Inflation fell sharply early in the month (1.7% in January after 2.0% in December), reinforcing the view that the ECB can stay on hold. On activity, the flash PMIs surprised slightly to the upside (composite at 51.9), mainly avoiding a rapid-cut scenario and helping stabilize the curve. Overall, EUR swap rates ended the month lower, with the 5-year EUR swap around 2.40%.

United Kingdom: The BoE kept its rate at 3.75%, but the vote split was notably tight (5–4), clearly putting a cut back on the table. At the same time, January inflation fell to 3.0%, even as domestic components remained under scrutiny (services around 4.4%). By month-end, Bailey summed it up plainly: a March cut is “a genuinely open question,” and it will depend on the next data releases.

Japan: In February, the key focus was the timing of the BoJ’s next steps (policy rate at 0.75%). On one hand, January core inflation returned to 2.0% (the lowest in two years), giving markets a reason to push back expectations of a near-term hike. On the other hand, the end of the month brought political and institutional signals seen as less supportive of a sustained tightening pace: a report about the Prime Minister’s reservations regarding further hikes, followed by the appointment of “reflationist” profiles to the BoJ’s Policy Board, which reduced expectations of a spring move.

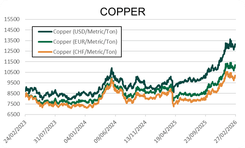

Commodities : Middle East tensions, oil on the rise

Oil: This month marked a clear return of an energy risk premium. In early February, Brent was still trading around $67/bbl, then rose steadily to $71–72/bbl, its highest level in seven months. The driver was rising tension around the US stance in the Middle East and the lead-up to talks with Iran. The two sides met on Thursday 26 February for a third round of nuclear talks that ended without an agreement; the mediator reported “progress,” and both parties agreed to continue with technical talks in Vienna next week.

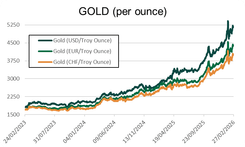

Gold: In February, precious metals were again highly volatile. After the late-January record above $5,500/oz, gold sold off early in the month, amplified by CME margin increases that forced position reductions. The second half then saw renewed buying: gold moved back toward $5,000/oz and then up to around $5,150–5,200/oz by late February, supported by “protection” demand when uncertainty rises, and intermittently capped by profit-taking whenever the dollar strengthens.

Silver: After peaking at $120/oz in January, silver corrected sharply early in the month. As with gold, CME margin increases forced position reductions, amplifying the downside movement. It traded around $95/oz at month-end, remaining highly volatile with even small shifts in market sentiment.

This market report was prepared on 02/27/2026, with certain data partially updated as of 03/02/2026 to reflect developments related to the situation in the Middle East

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.