Market Letter - June 2026

FX : a dominant dollar, with the euro weakened by three months of conflict

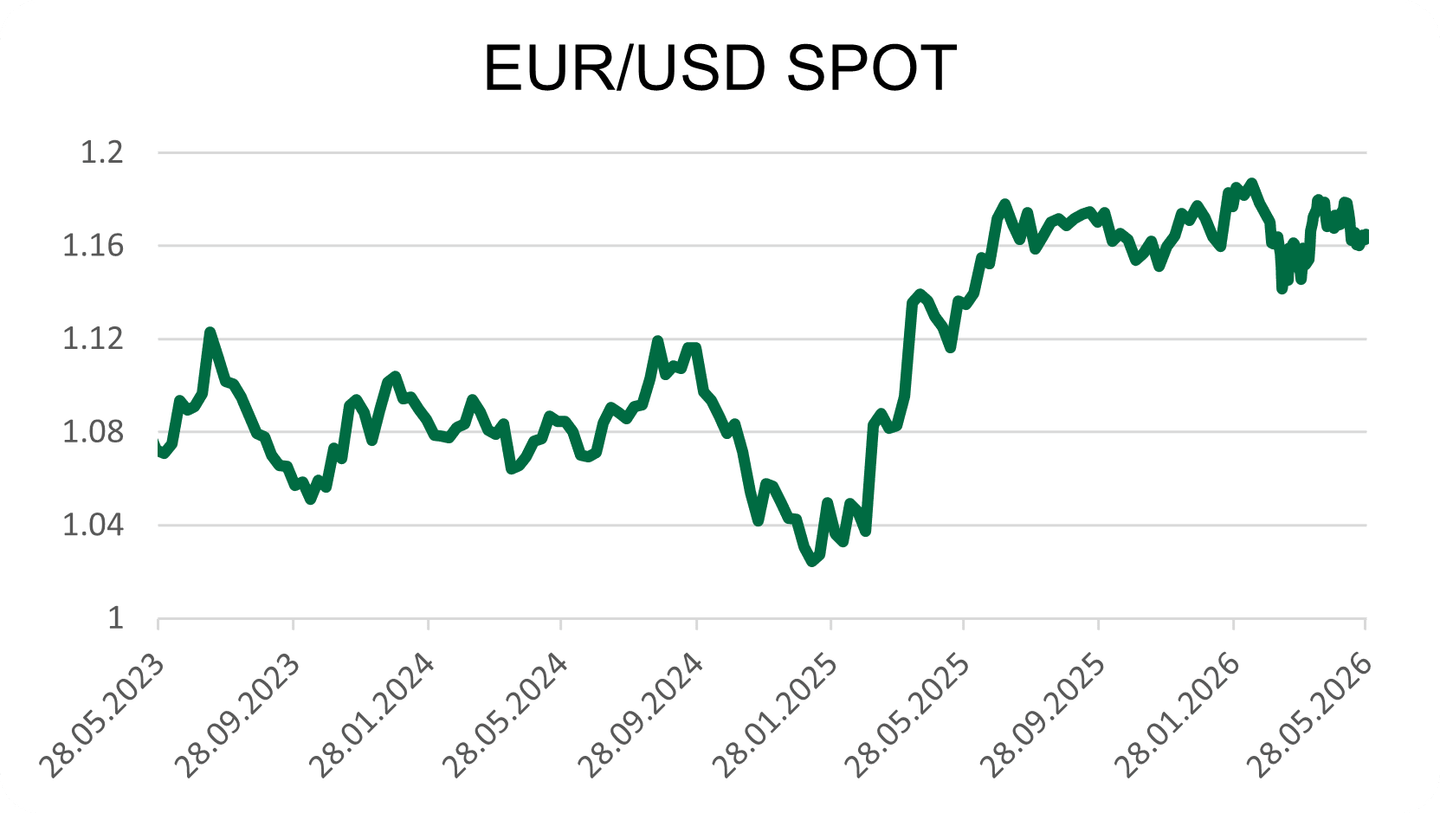

EURUSD: The EURUSD pair experienced a volatile month in May, driven by developments in the U.S.-Iran conflict and monetary policy expectations. The pair briefly rose above 1.1790 at the start of the month, supported by hopes of an agreement between the United States and Iran, before retreating towards 1.1720 and then around 1.1600/1.1630 over the month.

President Trump stated that an agreement with Iran had largely been negotiated and would be announced shortly, which temporarily supported the euro against the dollar amid improving risk appetite. However, these hopes were quickly tempered by a resumption of hostilities: U.S. strikes in Iran reignited risk aversion, strengthening demand for the safe-haven dollar and pushing EURUSD close to a six-week low.

Towards the end of the month, negotiations between Washington and Tehran appeared to be making progress, with a proposed 60-day agreement including an extension of the ceasefire, a resumption of talks on Iran’s nuclear programme and a gradual reopening of the Strait of Hormuz.

The dollar remains supported by elevated U.S. interest rates and stronger-than-expected inflation. However, renewed expectations of rate hikes in the euro area have allowed the euro to stabilise around 1.1650 against the dollar at the end of the period.

EURGBP: The pair reached 0.8720 in the middle of the month, against a backdrop of sterling weakness linked to political uncertainty following Labour’s underperformance and Keir Starmer’s interventionist speech. The latest UK data have reduced expectations of further rate hikes by the Bank of England: inflation slowed to 2.8% in April, from 3.3% in March, while the services PMI fell sharply to 47.9 in May, from 52.7 in April, pointing to a clear slowdown in activity. These factors limit the potential for further sterling appreciation, with EURGBP ending the month around 0.8670.

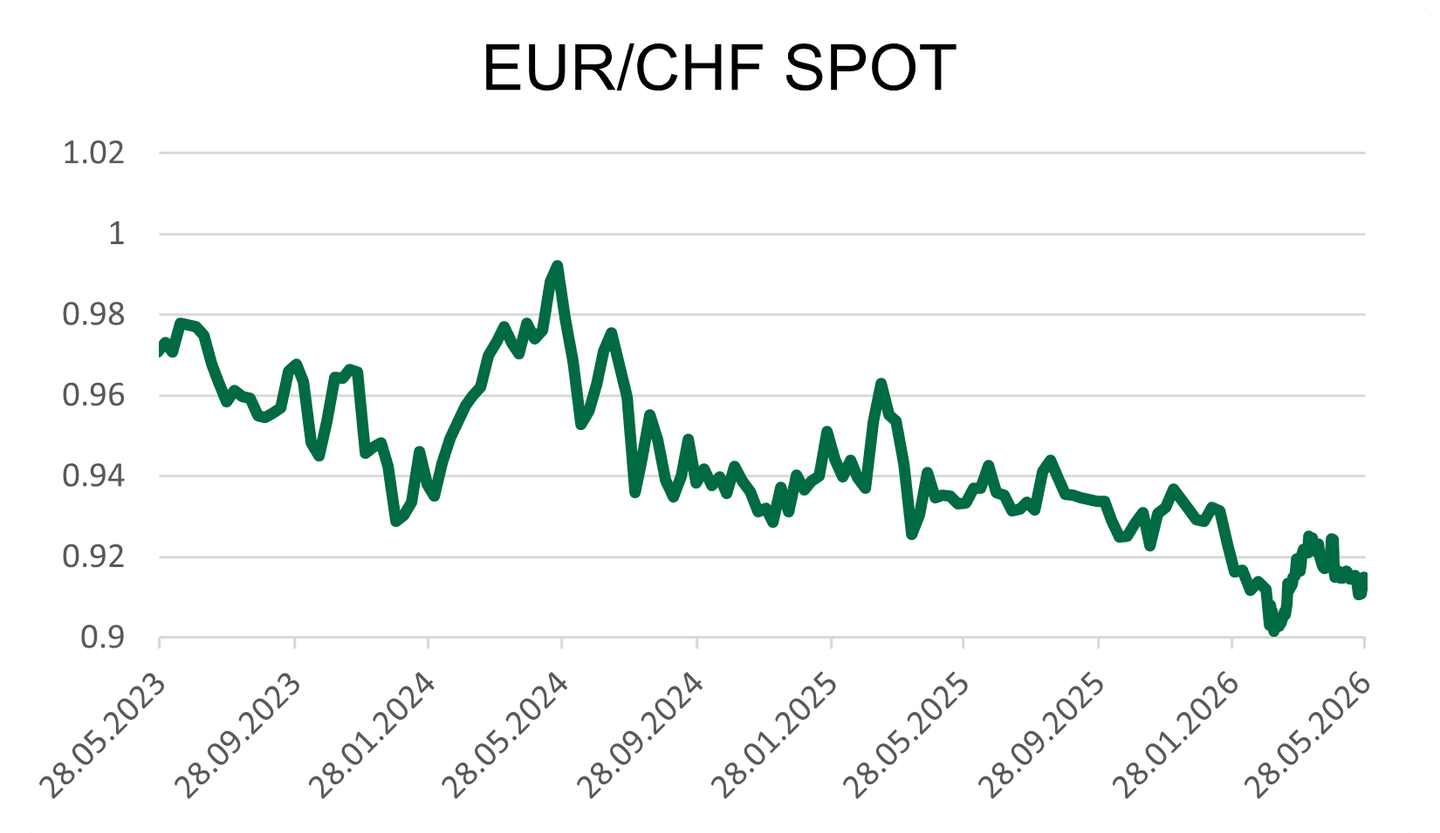

EURCHF: The pair traded between 0.9100 and 0.9170 over the month. EURCHF moved back towards 0.91 as renewed risk aversion linked to tensions in the Middle East and uncertainty around the Strait of Hormuz strengthened demand for the Swiss franc as a safe-haven currency.

Higher oil prices also weighed on the euro area’s growth outlook, limiting support for the euro. At the same time, franc appreciation remains contained by the Swiss National Bank’s vigilance, as the SNB could intervene in the event of a rapid move in order to avoid penalising the Swiss economy. The euro, for its part, continues to benefit from still-elevated rate expectations in the euro area.

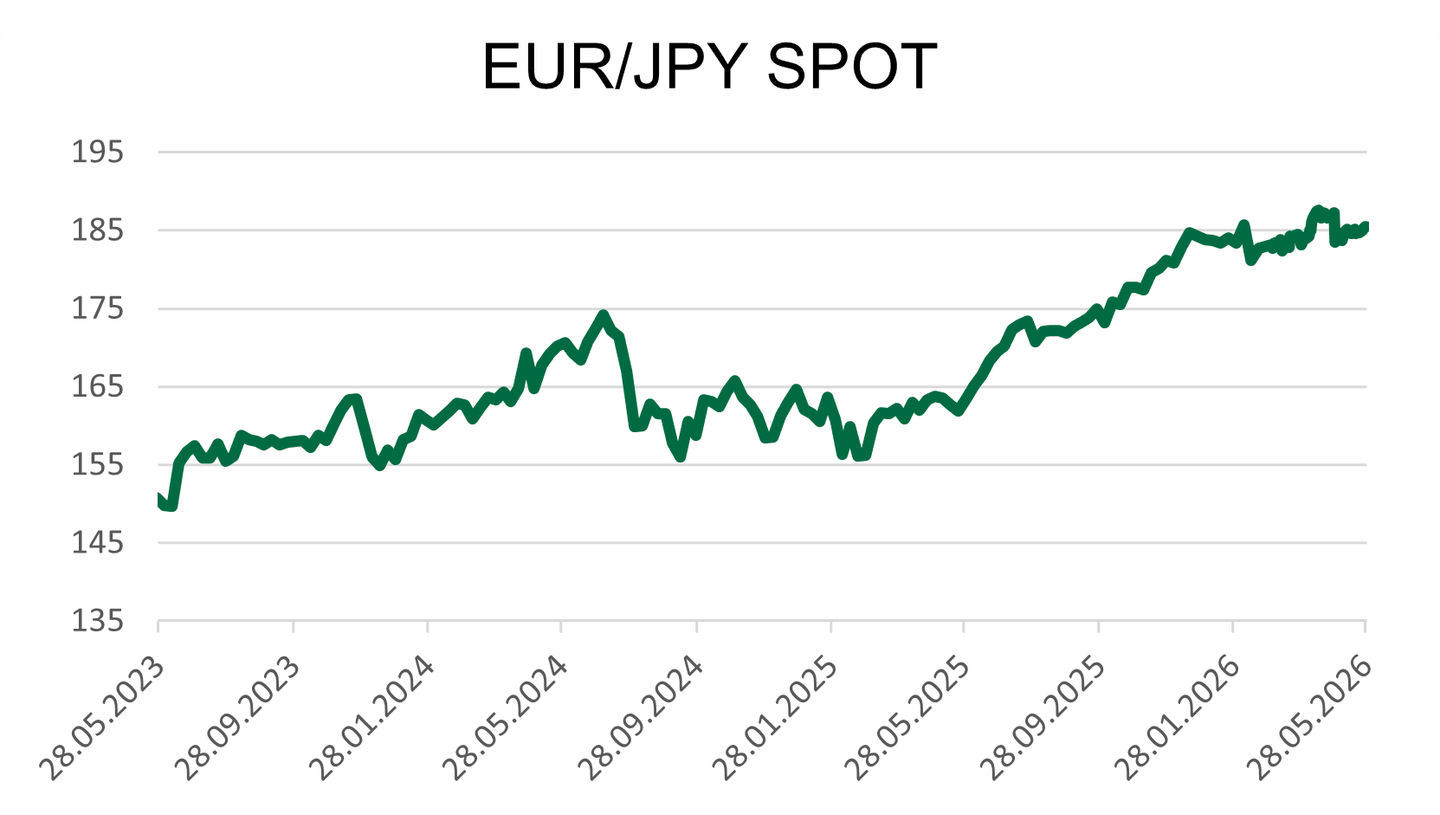

EURJPY: The pair traded around 185. It was supported by the euro and expectations of ECB rate hikes, while the yen remained weighed down by elevated oil prices, which are unfavourable for Japan’s energy-importing economy. Japanese authorities remain particularly attentive to currency movements. Finance Minister Satsuki Katayama warned that the government could take decisive action in the event of excessive volatility or speculative moves in the yen, amid speculation over a potential intervention in the foreign exchange market. At the same time, Bank of Japan Governor Kazuo Ueda also warned about inflationary risks linked to higher oil prices, without clearly signalling a rate hike at the next meeting.

Interest rates: central banks under pressure from renewed energy-driven inflation

United States: The Fed left its policy rates unchanged in May, but the acceleration in inflation reduced expectations of rapid rate cuts. Annual inflation came in at 3.8% in April, compared with 3.3% in March, mainly driven by higher gasoline prices linked to the conflict with Iran, while core inflation rose to 2.8%. Core PCE, the Fed’s preferred measure of underlying inflation, increased by 0.2% month-on-month in April and by 3.3% year-on-year, remaining well above the 2% target. These figures, combined with a still-resilient labour market, with 115,000 jobs created and unemployment stable at 4.3%, limit the Fed’s room for manoeuvre. The end of the month was also marked by Kevin Warsh taking office as Fed Chair, replacing Jerome Powell, who remains a governor. The Fed Minutes show a divided central bank: several members believe that a rate hike could become necessary if inflation remains persistently above 2%, while others remain open to rate cuts if inflation slows more clearly or if the labour market deteriorates.

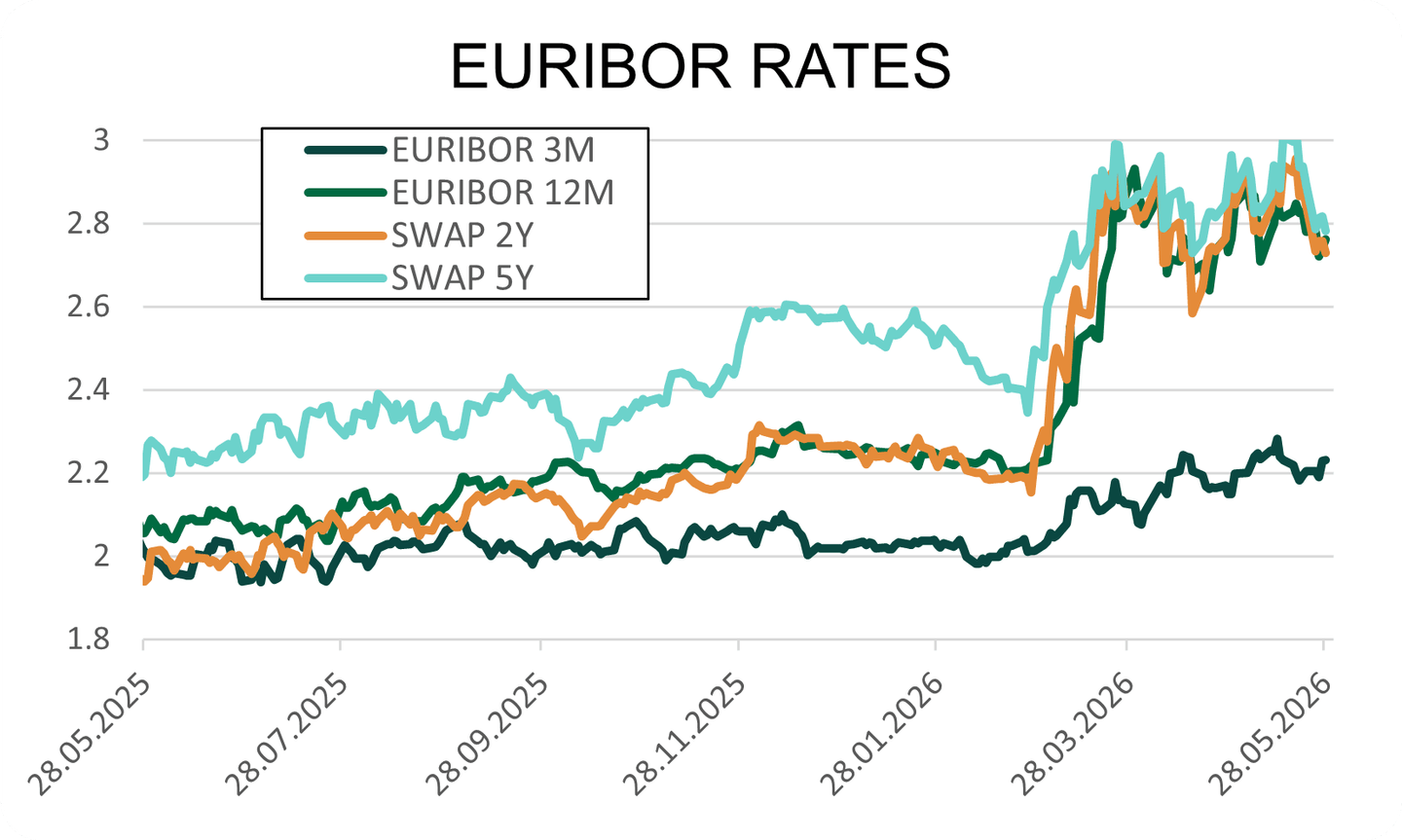

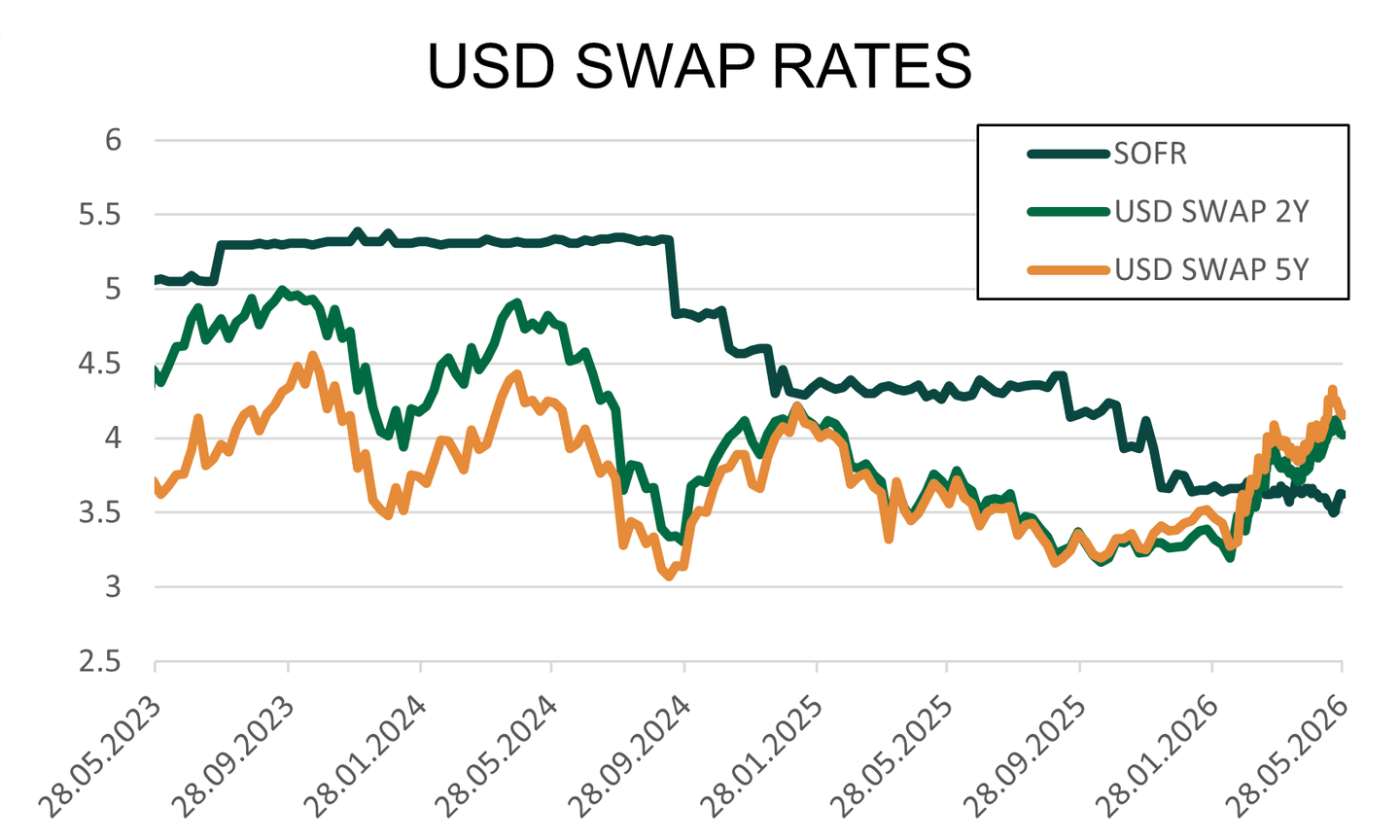

Euro area: The ECB kept its policy rates unchanged in early May, but its tone hardened significantly in response to renewed inflationary pressures. Philip Lane, the ECB’s Chief Economist, and Isabel Schnabel, a member of the ECB Executive Board, both warned that inflationary pressures were currently stronger than expected in the latest March projections. The ECB could therefore revise its inflation forecasts upwards at its 11 June meeting. Isabel Schnabel notably stated that a rate hike in June would be necessary, even in the event of a peace agreement with Iran, arguing that the energy shock remains too persistent to be ignored. The latest French inflation figures reinforced this view: annual inflation rose to 2.2% in April, from 1.7% in March, mainly driven by energy, while harmonised European inflation reached 2.5%, moving back above the ECB’s 2% target for the first time since August 2024. Money markets are now pricing in two ECB rate hikes this year. In this context, the 2-year EUR swap rate stands at around 2.72%, while the 5-year EUR swap rate is around 2.78%.

Japan: The Japanese economy surprised positively in Q1 2026, with GDP growth of 0.5% quarter-on-quarter, supported by a recovery in private consumption, higher public investment and, above all, resilient exports. Foreign trade improved significantly in April, with a surplus of JPY 301.9bn, supported by a 14.8% increase in exports, particularly to China, the United States, ASEAN and the European Union. At the same time, inflation slowed to 1.4% in April, as did core inflation, now below the BoJ’s 2% target, reducing short-term pressure for a rapid rate hike. However, the Bank of Japan remains cautious: higher energy prices linked to the Middle East conflict, combined with yen weakness, could reignite inflationary pressures in the coming months. In this context, the BoJ is expected to maintain a tightening bias, although the timing will remain highly dependent on developments in oil prices, the yen and domestic demand.

United Kingdom: UK rates fluctuated significantly during the month. At the beginning of the period, gilts were under pressure, with the 10-year yield around 5.12% and the 30-year yield at 5.80%, amid elevated expectations of further Bank of England rate hikes. Sterling was also affected by political uncertainty following Labour’s underperformance in local elections and Keir Starmer’s more interventionist speech, which revived questions about the country’s fiscal direction. Towards the end of the month, the latest data changed market perceptions: inflation slowed to 2.8% in April, while the services PMI fell sharply to 47.9 in May, from 52.7 in April, pointing to a clear slowdown in activity. These elements reduce the pressure on the Bank of England to continue raising rates. In this context, UK yields fell significantly: the 10-year gilt yield declined to 4.80%, while the 30-year yield moved down to 5.52%.

Commodities: Brent lower on the back of negotiations, but uncertainty remains persistent

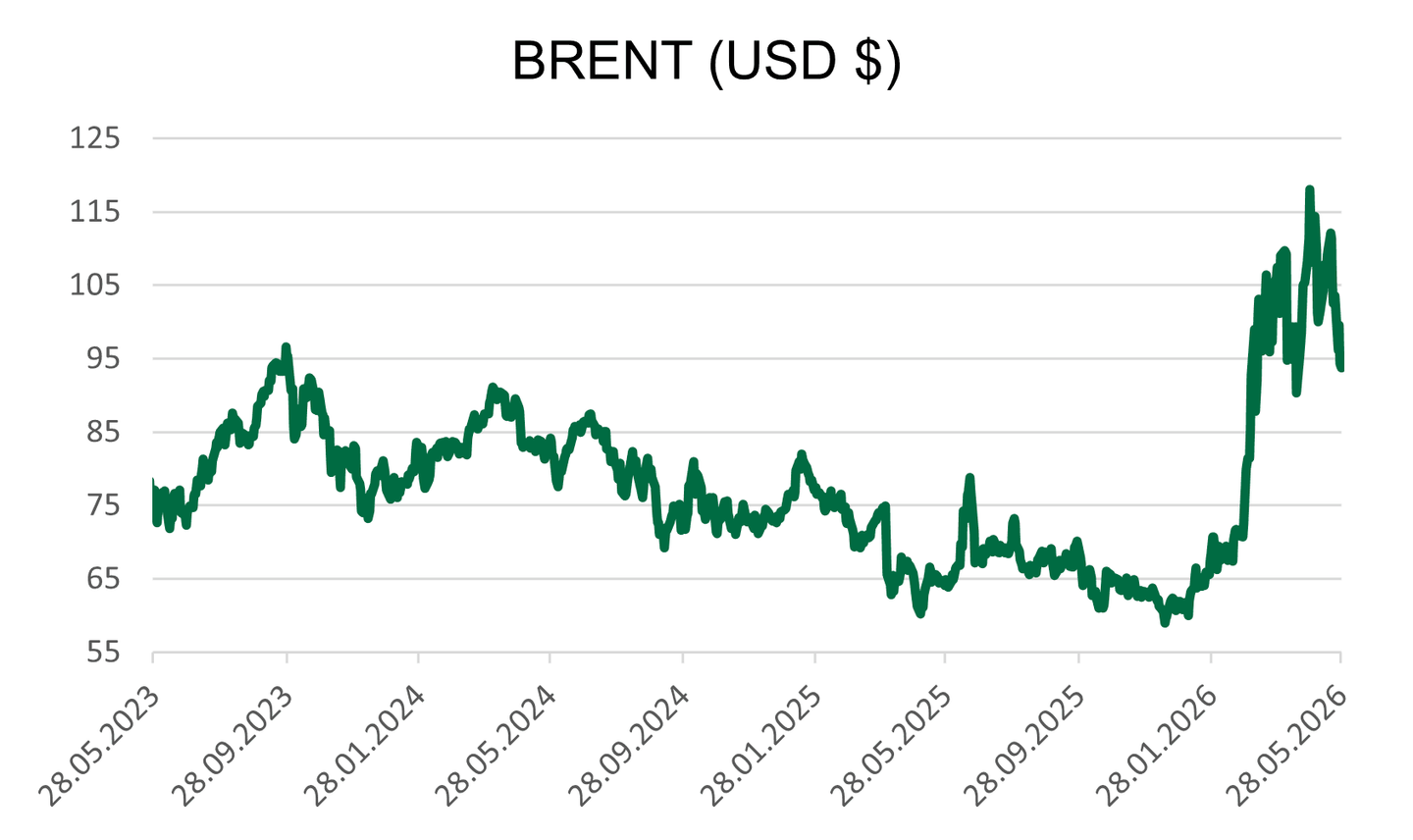

Oil: Brent experienced a highly volatile month. It rose above USD 110 at the beginning of the month due to the blockade of the Strait of Hormuz, before retreating. At least 33 oil tankers, including large tankers, crossed the strait with Iran’s authorisation, while around 240 vessels were still waiting to pass through. The agreement under discussion provides for a 60-day extension of the ceasefire, a gradual reopening of the Strait of Hormuz and a de-escalation of maritime tensions over the first 30 days, alongside negotiations on Iran’s nuclear programme. In this context, Brent fell back below USD 92 per barrel at the end of the month. However, Trump warned that unresolved issues include Iran’s frozen assets and its reluctance to guarantee unrestricted passage through Hormuz.

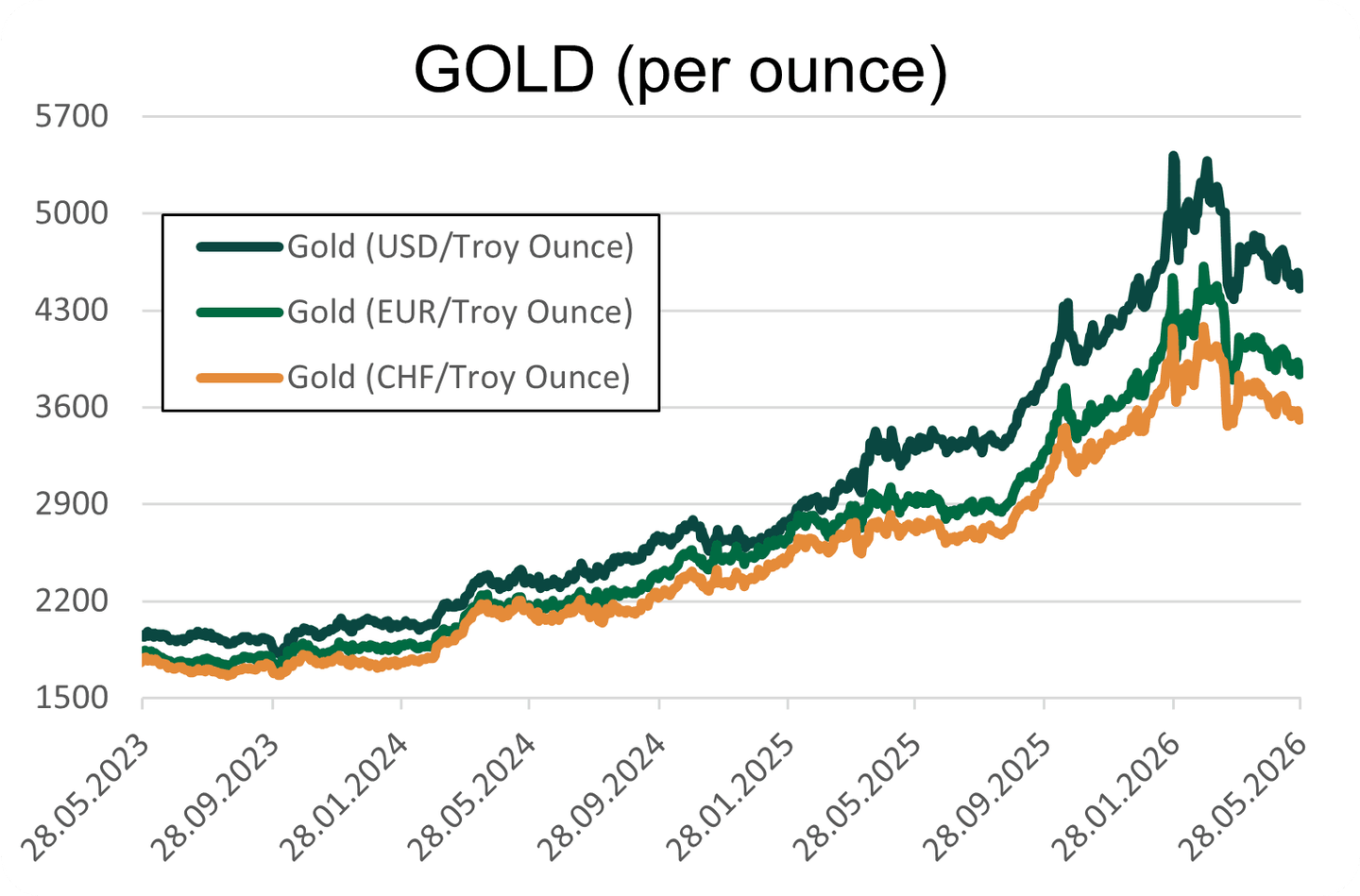

Gold: Gold traded between USD 4,500 and USD 4,660 per ounce before falling back below USD 4,400 at the end of the month, reaching a two-month low. It then stabilised around USD 4,500 per ounce, caught between support from geopolitical uncertainty and pressure from elevated U.S. rates and a strong dollar. Prices therefore remain around 15% below their levels at the start of the conflict, as expectations of restrictive monetary policy continue to weigh on the metal.

Silver: Silver also fluctuated sharply, after reaching a two-month high near USD 87 per ounce, before falling back below USD 76 at the end of the month. The metal retains medium-term support thanks to its industrial component, but remains sensitive to movements in the dollar, U.S. rates and the level of geopolitical risk.

This market report was prepared on 05/29/2026

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.