Market Letter - July 2026

Currencies: dollar surges amid restrictive Fed policy and easing geopolitical tensions

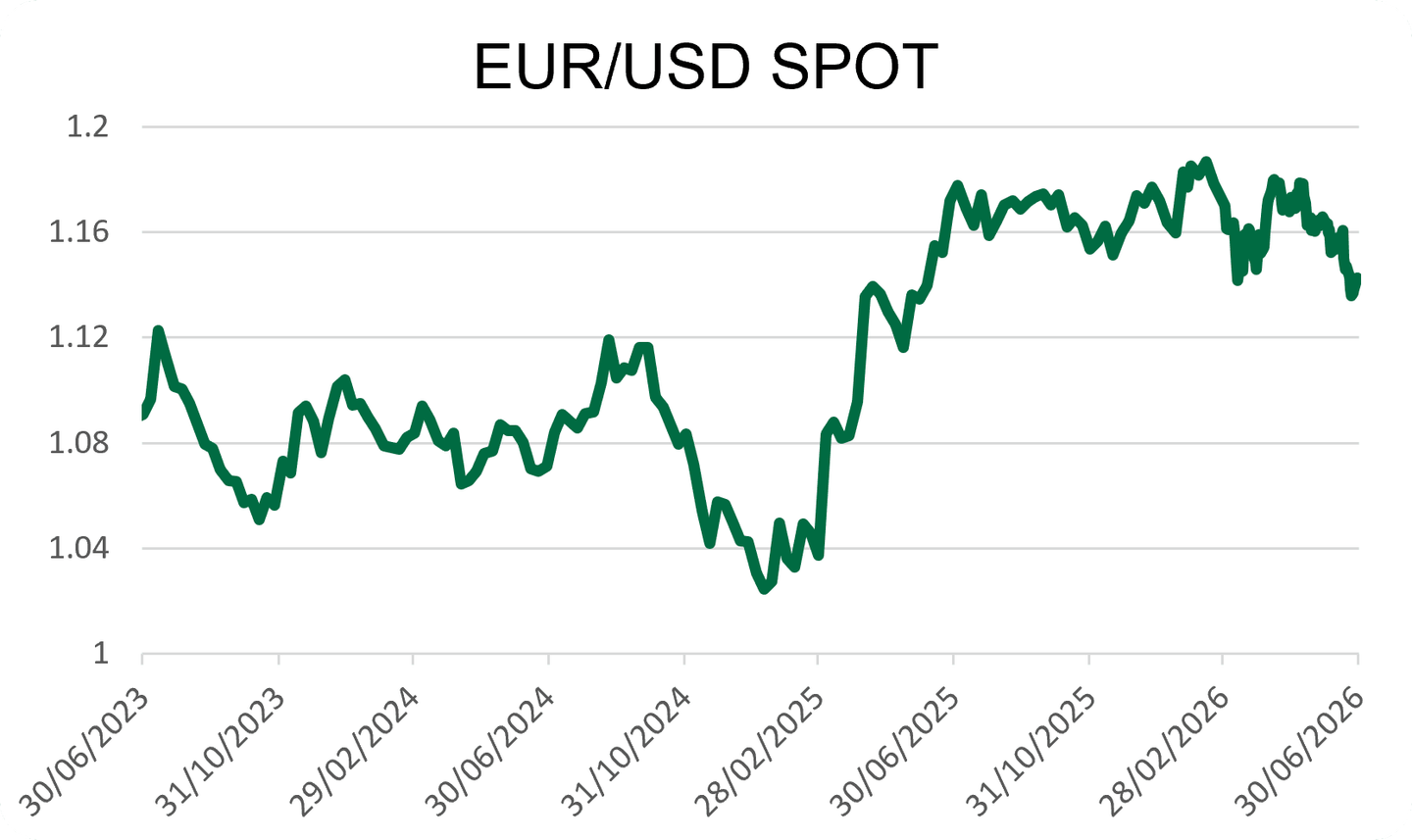

EURUSD: In June, EURUSD fell sharply. The pair was trading around 1.1650 at the beginning of the month; after hitting a low of 1.1350, it is now trading around 1.14. This rise in the dollar came after the Fed kept rates unchanged in the 3.50%–3.75% range, with US inflation still high at 4.2% year-on-year in May. Kevin Warsh’s very hawkish speech suggested that a rate hike remains possible later this year. The dollar index rose by around 2.5% in June and is now close to a thirteen-month high.

Geopolitics also supported the dollar. Tensions between the United States and Iran strengthened demand for the dollar as a safe-haven currency, even though the partial resumption of flows through the Strait of Hormuz later reduced pressure on oil prices.

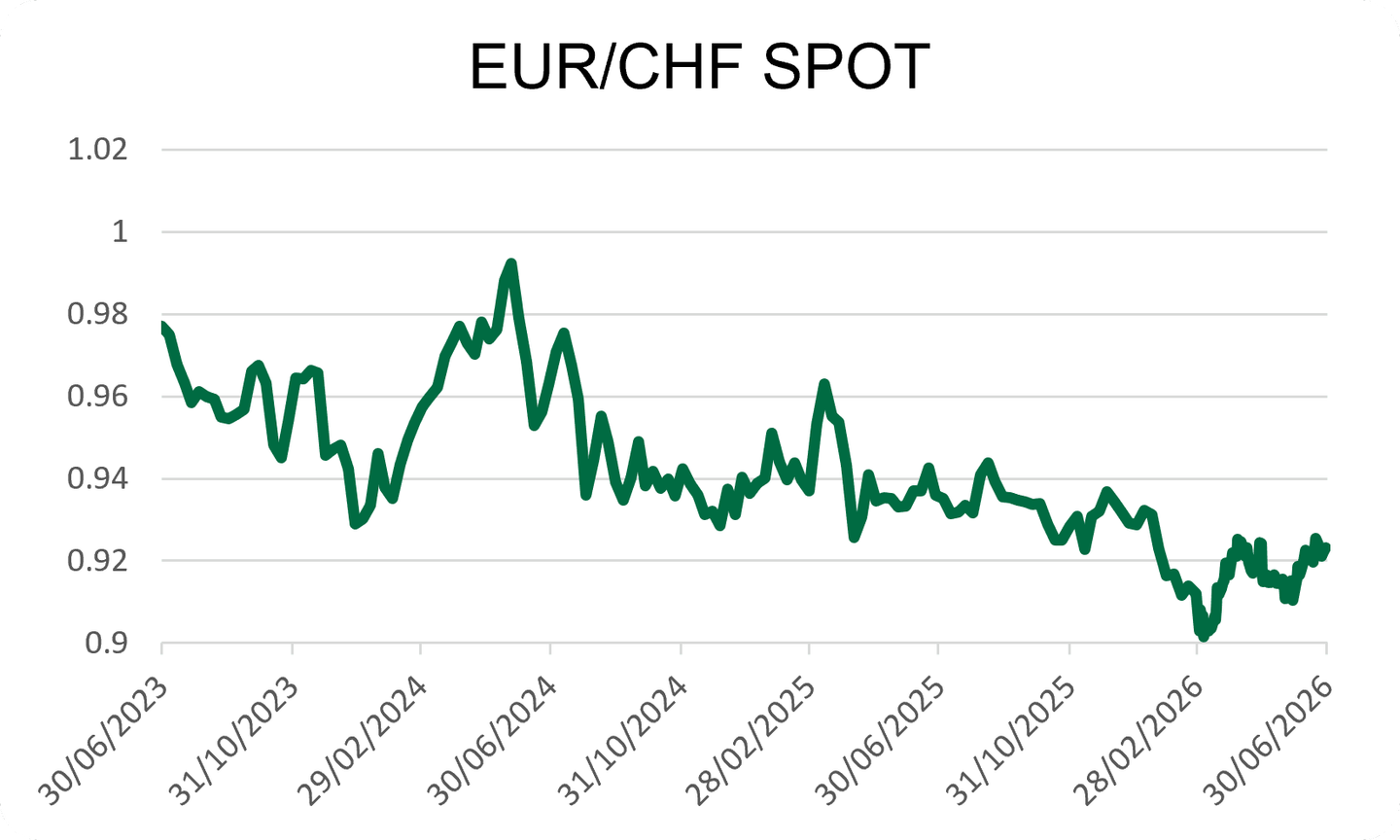

EURCHF: EURCHF remained relatively stable in June, around 0.92–0.93. The pair stood at 0.926 at the end of the month before moving back toward 0.922, with the Swiss franc remaining firm but without a strong appreciation move. Despite tensions in the Middle East, the CHF did not benefit significantly from its safe-haven status.

This stability can partly be explained by the decline in oil prices from their spring highs. As long as energy prices remain contained and flows through the Strait of Hormuz gradually resume, the perception of geopolitical risk decreases and makes the Swiss franc less attractive, given its near-0% rate environment. The CHF nevertheless retains its role as a hedge in the event of geopolitical stress. A renewed rise in oil prices or a more prolonged blockage of the Strait of Hormuz could therefore quickly revive demand for the Swiss franc and put renewed pressure on EURCHF.

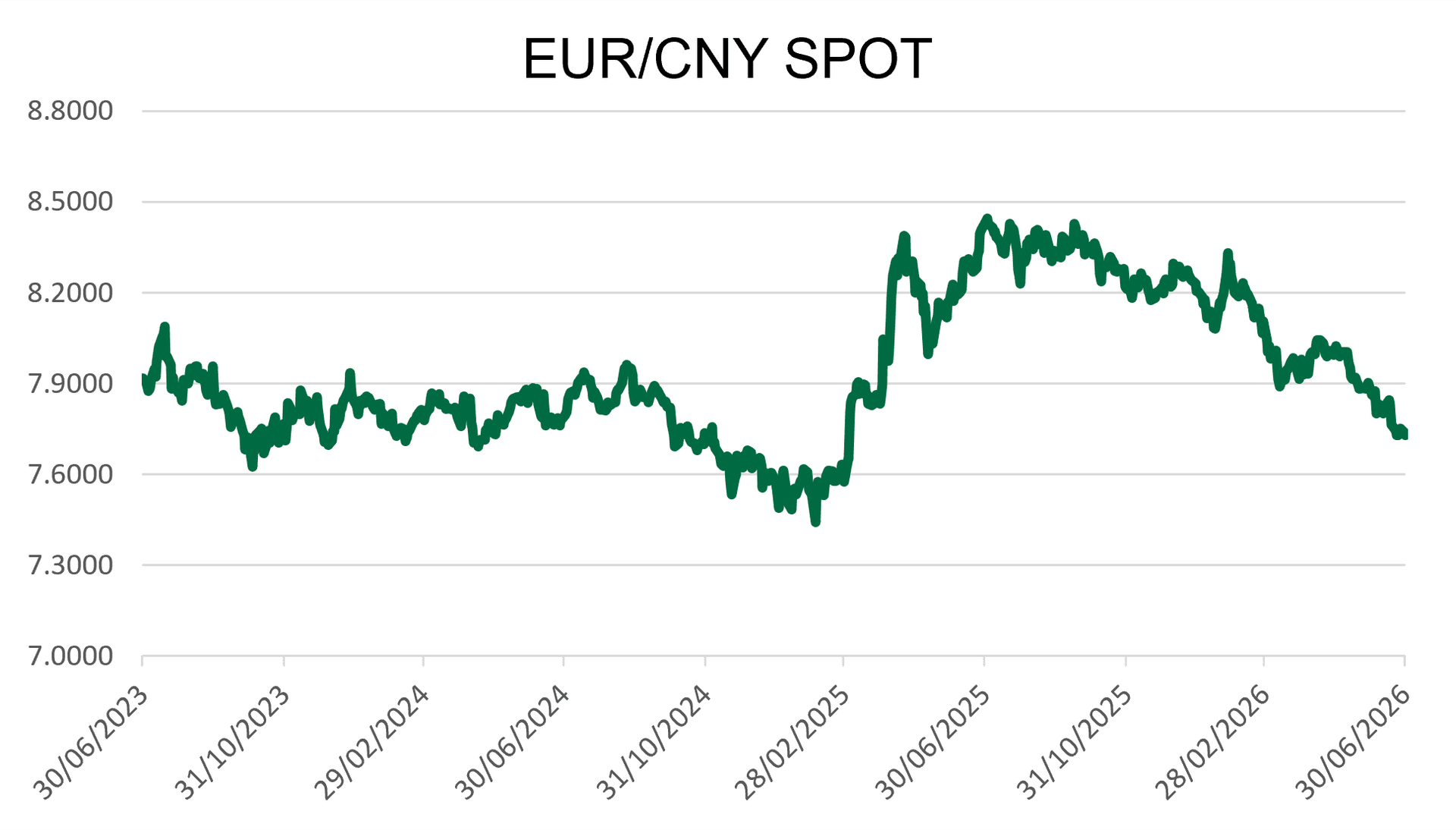

EURCNY: The Chinese yuan has risen by more than 5% against the euro since January 1, from around 8.20 to 7.72, with EURCNY falling by 2.3% in June.

This appreciation of the yuan has a commercial dimension. A stronger CNY reduces the price advantage of Chinese exporters. It can be interpreted as a signal of monetary stabilization sent to the United States, in a context where Sino-American trade relations remain tense. Beijing is not allowing its currency to weaken in order to support exports; on the contrary, a firmer yuan helps limit criticism over the undervaluation of the Chinese currency.

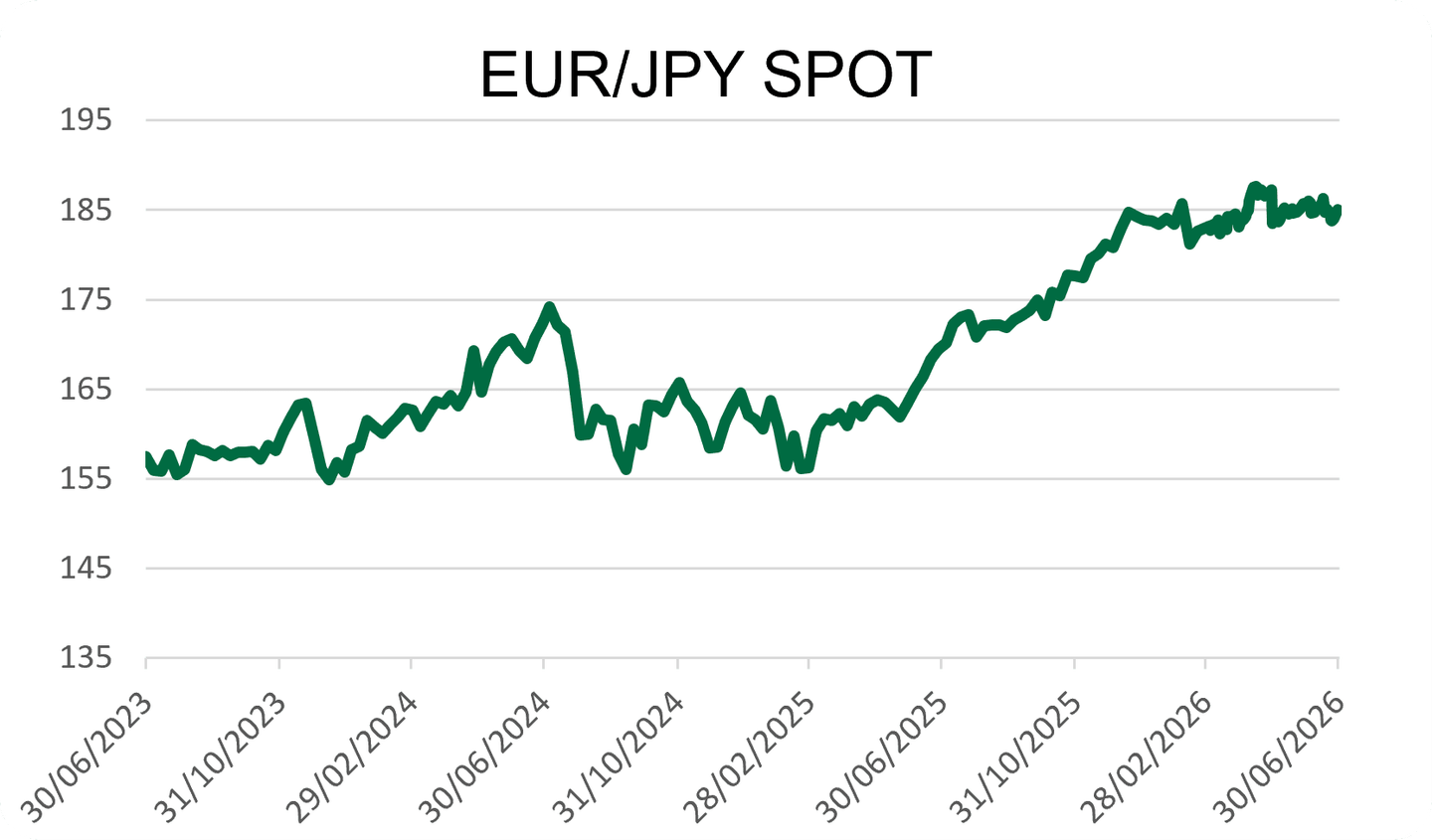

EURJPY: EURJPY remains at historically high levels. Despite the Japanese government’s many attempts to revive the yen, the Japanese currency continues to trade near its lowest levels in 40 years.

Yen weakness remains the central factor. The Bank of Japan raised its policy rate to 1.00%, its highest level since 1995. Despite this, the yen has not rebounded strongly because the interest-rate gap with Europe and the United States remains significant. The ECB deposit rate is at 2.25%, and the Fed is at 3.50%–3.75%. The yen therefore remains penalized by Japanese rates that are still lower than European and US rates.

Japan is also a net energy importer. Higher oil and LNG prices therefore weigh on its trade balance. When energy prices rise, Japan has to buy more foreign currency to pay for its imports, which weighs on the yen.

Interest rates: ECB raises rates as central banks remain cautious on inflation

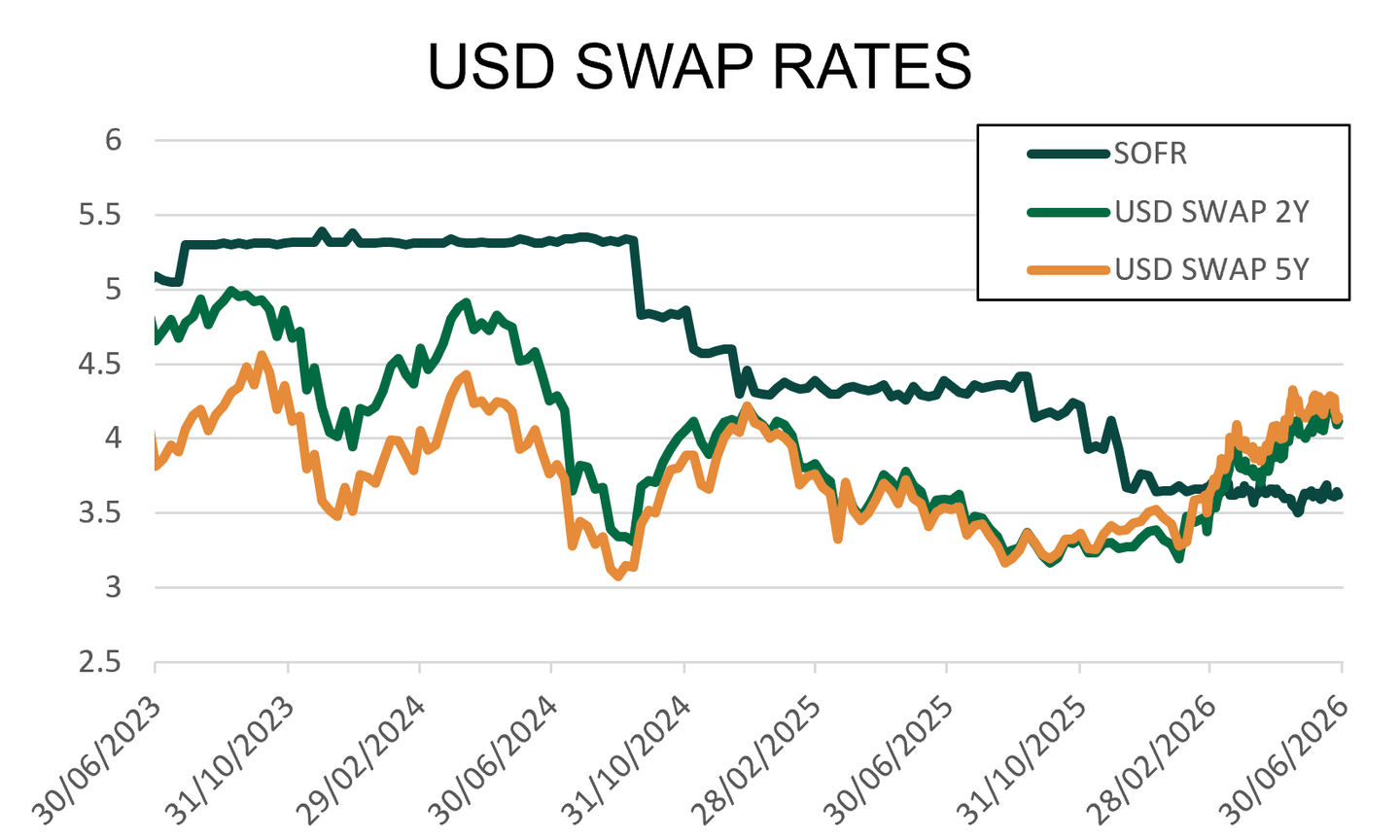

United States: The Fed kept rates unchanged in June, in the 3.50%–3.75% range. This decision does not amount to monetary easing: rates remain high and the central bank has not yet given a clear signal of a rapid cut. The market is mainly watching inflation trends, energy prices and comments from Fed members.

US inflation remains high, with CPI up 0.5% month-on-month and 4.2% year-on-year in May. The increase was largely driven by energy, which contributed strongly to the monthly rise in prices. By contrast, inflation excluding food and energy remains more moderate, at 2.9% year-on-year. This shows that inflationary pressure is still present, but that it is mainly being driven by energy prices rather than by a broad-based acceleration in prices.

Market inflation expectations remain more contained, however. US breakevens have fallen from their March-April peaks, with the 5-year breakeven inflation rate around 2.21% and the 10-year around 2.20% at the end of June. This is an important signal: even though realized inflation remains high, markets are not yet pricing in a scenario where inflation stays sustainably above 4%. This currently limits the rise in long-term rates, but the Fed should remain cautious as long as energy and prices remain volatile.

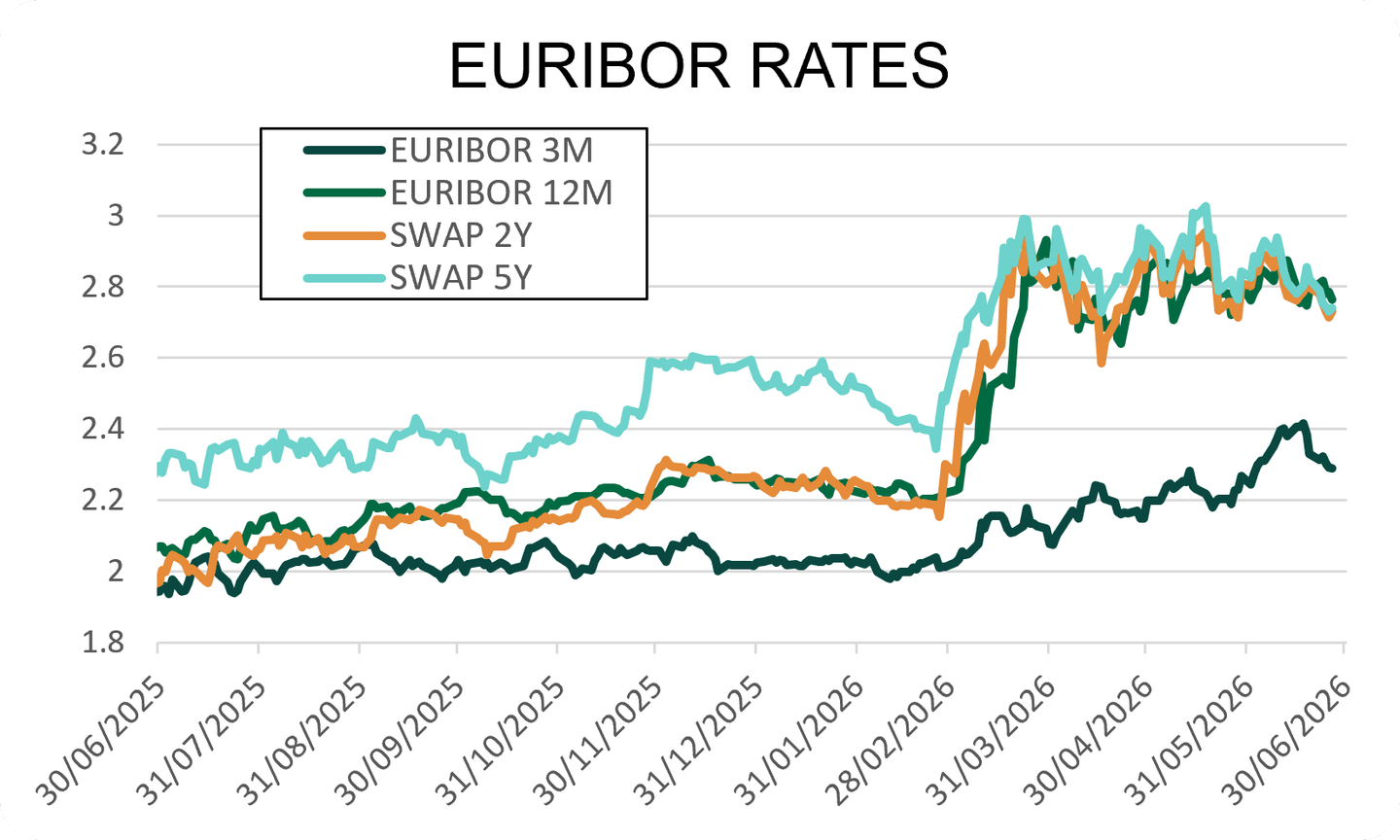

Eurozone: The ECB raised its rates by 25 basis points on June 11. The deposit rate rose to 2.25%, the refinancing rate to 2.40% and the marginal lending rate to 2.65%. This decision reflects persistent inflationary pressures in the eurozone: the ECB raised its inflation forecasts, now expecting inflation at 3.0% in 2026, 2.3% in 2027 and 2.0% in 2028, mainly due to higher energy prices and their possible pass-through to food prices, goods and services.

However, the latest figure published in France shows a sign of easing, with inflation slowing in June. This decline nuances the overall diagnosis: it suggests that price pressures are not spreading evenly across the entire eurozone, even though the ECB remains cautious about the risk of persistent inflation.

For companies, the main risk is therefore not only the current level of rates, but also the possibility of having to deal with higher financing costs for longer, particularly for debt indexed to Euribor.

United Kingdom: The Bank of England kept its policy rate at 3.75% in June, despite a split vote within the committee: seven members voted for no change and two voted for a hike to 4.00%. This decision reflects inflation that remains above target, at 2.8% in May, even though it remains contained. The recent decline in oil prices reduces the immediate risk, but energy prices remain a key point to watch in the coming months. For companies exposed to sterling, this stability supports EURGBP, while the cost of GBP financing remains high. The main risk would be a rebound in inflation, which could revive the prospect of further monetary tightening.

Japan: The Bank of Japan raised its policy rate to 1.00%, from 0.75% previously. This is the highest level since 1995 and confirms the BoJ’s willingness to continue gradually normalizing monetary policy after several years of very low rates. The increase remains cautious, however, as the central bank wants to avoid tightening too abruptly and weakening economic activity.

Despite this increase, Japanese rates remain below those of other major economies. The yield gap with the United States, the eurozone and the United Kingdom therefore remains significant, limiting the yen’s attractiveness for investors. This is why the rise in Japanese rates has not been enough to trigger a marked recovery in the currency.

The BoJ also has to deal with rising energy costs. Japan imports a large share of its oil and LNG needs, making its economy sensitive to tensions in energy prices. More expensive energy can fuel imported inflation and weigh on both households and companies. The Bank of Japan is therefore moving cautiously: it must support the credibility of the yen and contain inflation, without slowing growth too sharply.

China: The People’s Bank of China kept its main benchmark rates unchanged in June, with the one-year LPR at 3.00% and the five-year LPR at 3.50%. Monetary policy therefore remains accommodative, but without a new rate cut for now. The PBoC is instead prioritizing liquidity support, particularly through short-term refinancing operations, to stabilize the money market. For companies, the cost of CNY financing remains relatively favorable, but the main risk comes from slowing domestic demand, persistent tensions in real estate and movements in the yuan, which limit the central bank’s room for manoeuvre.

The June LPR figures were kept at 3.00% and 3.50%, while the seven-day repo rate, the main monetary policy rate, remained at 1.40%.

Commodities: Oil returns to pre-conflict levels, but uncertainty remains

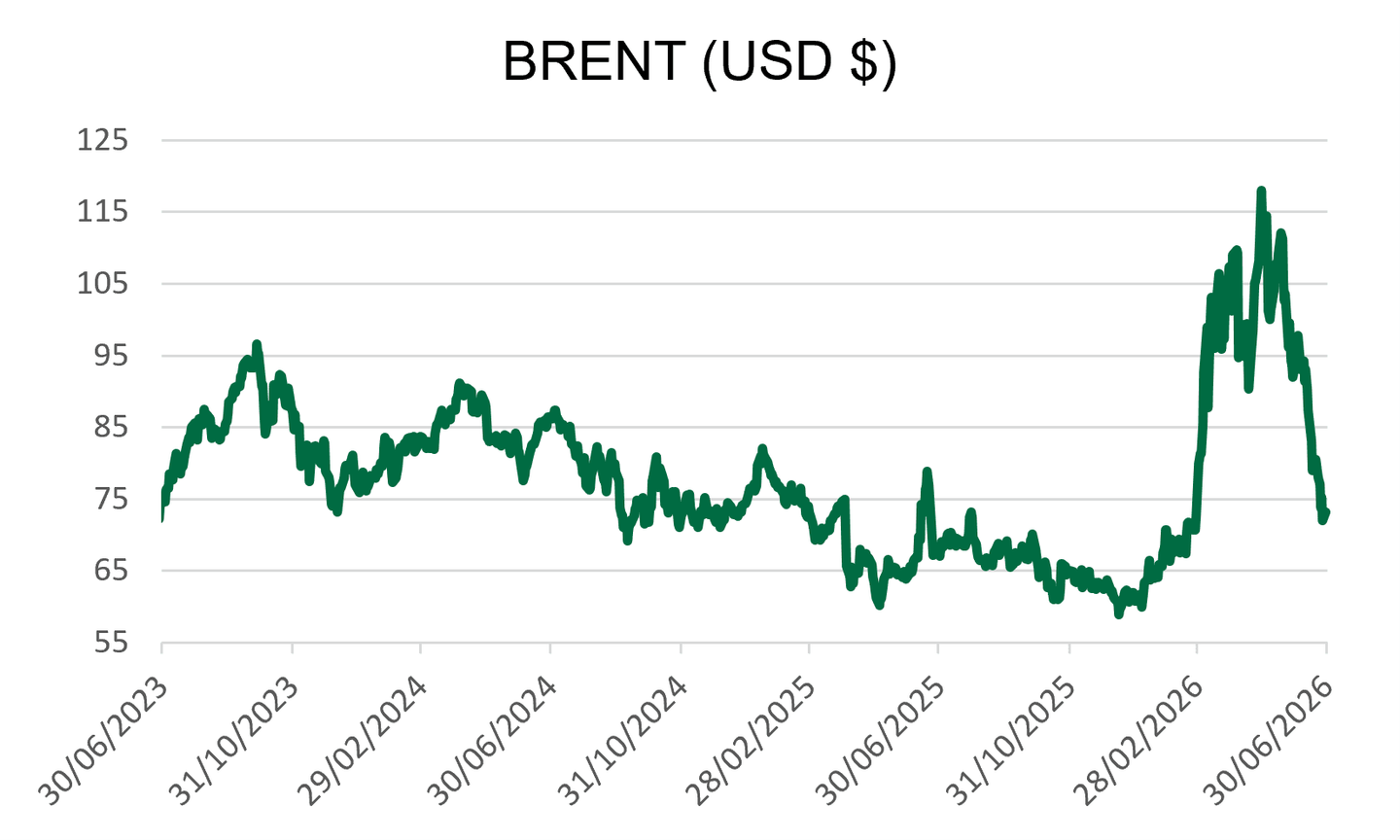

Oil: Oil fell sharply in June. Brent returned to around USD 72–73 per barrel at the end of the month, its lowest level since February 27, before the start of the war with Iran.

The move was driven by the partial resumption of flows through the Strait of Hormuz. Around 20 million barrels passed through the strait in one day around June 24, and several blocked tankers started moving again. The market therefore shifted from an immediate shortage scenario to a scenario of gradual supply recovery. Brent lost more than 10% over one week and more than 20% compared with levels at the beginning of the month.

The decline in oil prices is positive for energy importers and for companies exposed to transport, chemicals, plastics and logistics. But the risk has not disappeared. Flows are resuming, but infrastructure remains fragile and the situation between the United States and Iran has not stabilized. Any renewed disruption in Hormuz could quickly push prices higher again.

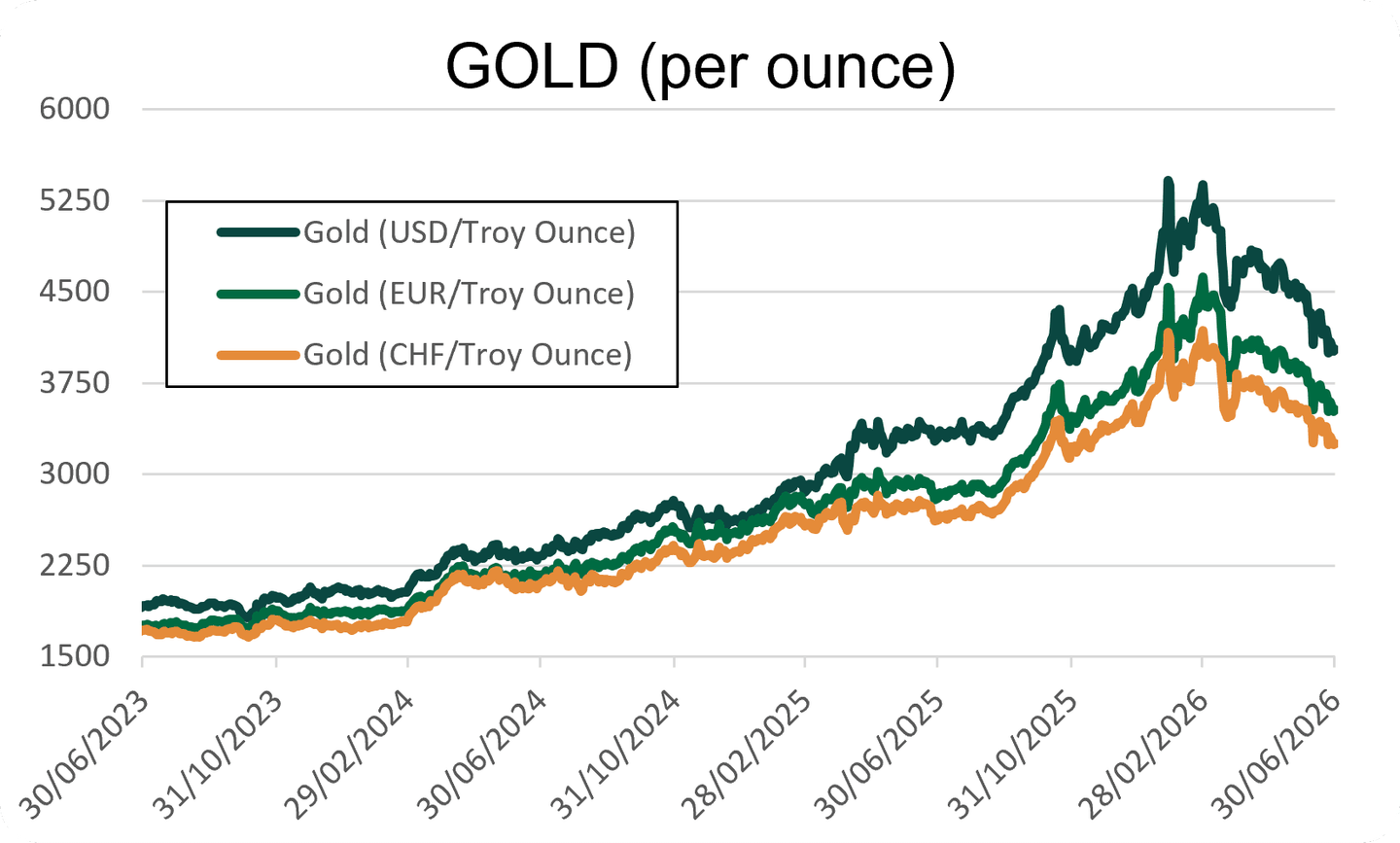

Gold: Gold fell sharply in June and is trading around USD 4,050 per ounce at the end of the month. Over the month, the decline is around 10.5%, confirming a clear drop in appetite for the precious metal despite a still uncertain geopolitical backdrop. The move is mainly explained by the stronger dollar and the continuation of high interest rates in the United States.

When the dollar appreciates, gold becomes more expensive for buyers outside the dollar zone, which weighs on demand. At the same time, high rates make bonds and money-market investments more attractive than gold, which does not pay interest. Gold’s safe-haven status was therefore not enough to offset the negative effect of a strong dollar and high yields. As long as the Fed maintains a restrictive tone and expectations of rate cuts remain limited, gold may remain under pressure.

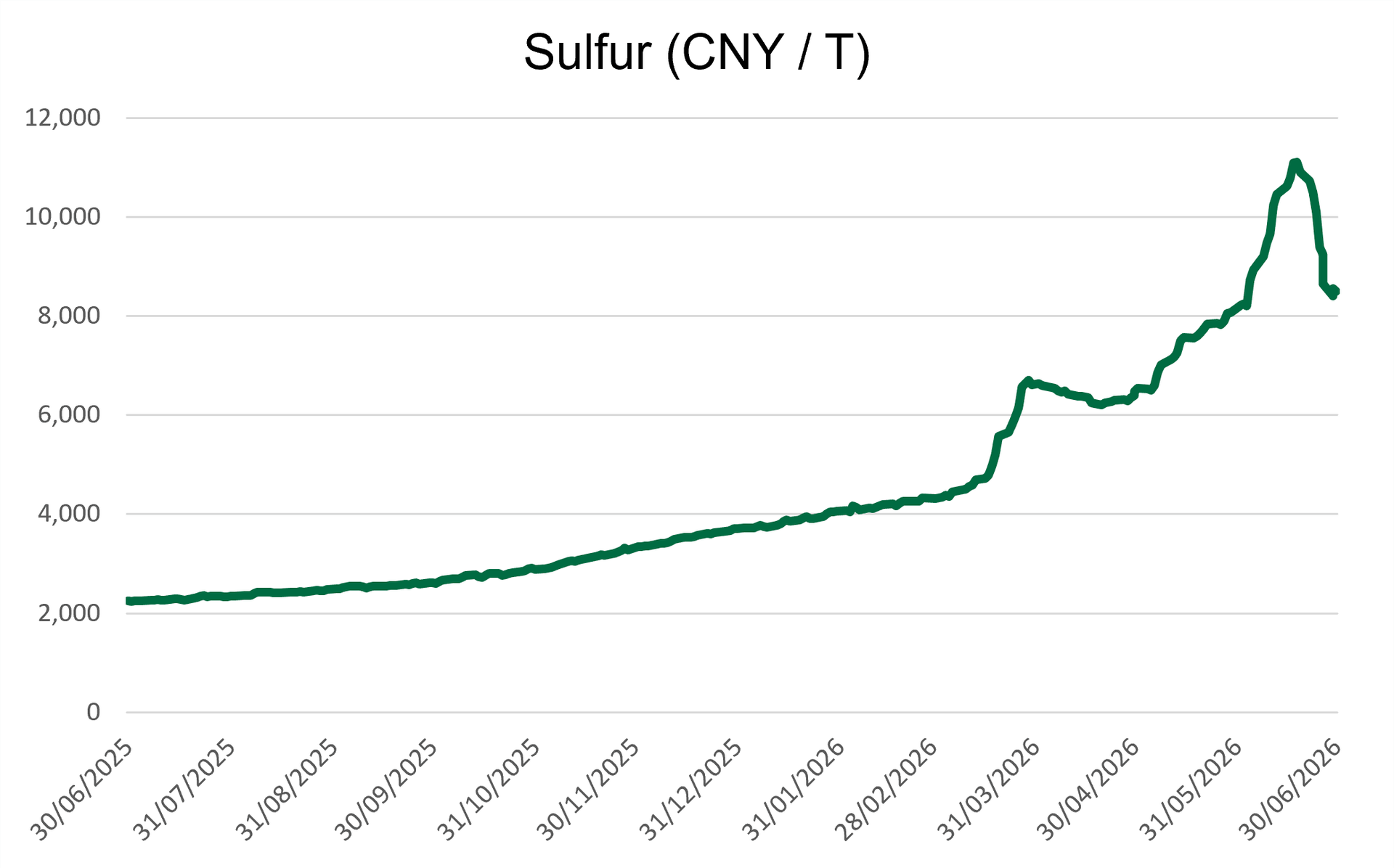

Sulphur: Sulphur was one of the most significant moves of the month. The price stood at CNY 8,401 per tonne on June 26. It fell by 8.46% on the day, but remains up 12.01% over one month and 259.89% year-on-year. Sulphur also reached an all-time high in June, at CNY 11,084 per tonne.

This is important because sulphur is a key input for sulphuric acid. Sulphuric acid is used in fertilizers, but also in some industrial chains linked to copper and nickel. Before the war, nearly half of global seaborne sulphur transited through the Strait of Hormuz. The partial blockage of the strait therefore directly affected the fertilizer supply chain.

Since the interim agreement of June 15, around 640,000 tonnes of sulphur and 427,000 tonnes of urea have left the strait. This is much more than during the conflict period, but volumes remain below normal.

For agricultural, chemical and mining companies, the signal is negative: sulphur remains very expensive. This may maintain pressure on fertilizer costs and on some industrial chains. The temporary decline at the end of June is not enough to offset the annual increase.

Natural gas / LNG: LNG remains expensive. Asian prices have risen by around 75% since the start of the conflict with Iran and stood at around USD 18.20 per mmBtu in early June. The March peak reached USD 25.30 per mmBtu after attacks on Qatari infrastructure. The market has therefore fallen from its peak, but it remains well above pre-war levels.

The reason is simple: the Gulf remains central to global LNG. Tensions around Hormuz directly affect export routes, particularly for Qatar. At the same time, Asian demand is recovering with warmer weather and inventory rebuilding. Japan and China are returning to the market, which limits the decline in prices.

For European companies, Asian LNG is not always the price paid directly, but it influences the global gas market. When Asia pays more, available cargoes for Europe become more expensive. Gas-intensive industries: chemicals, fertilizers, glass, paper, agri-food; therefore remain exposed to high energy costs.

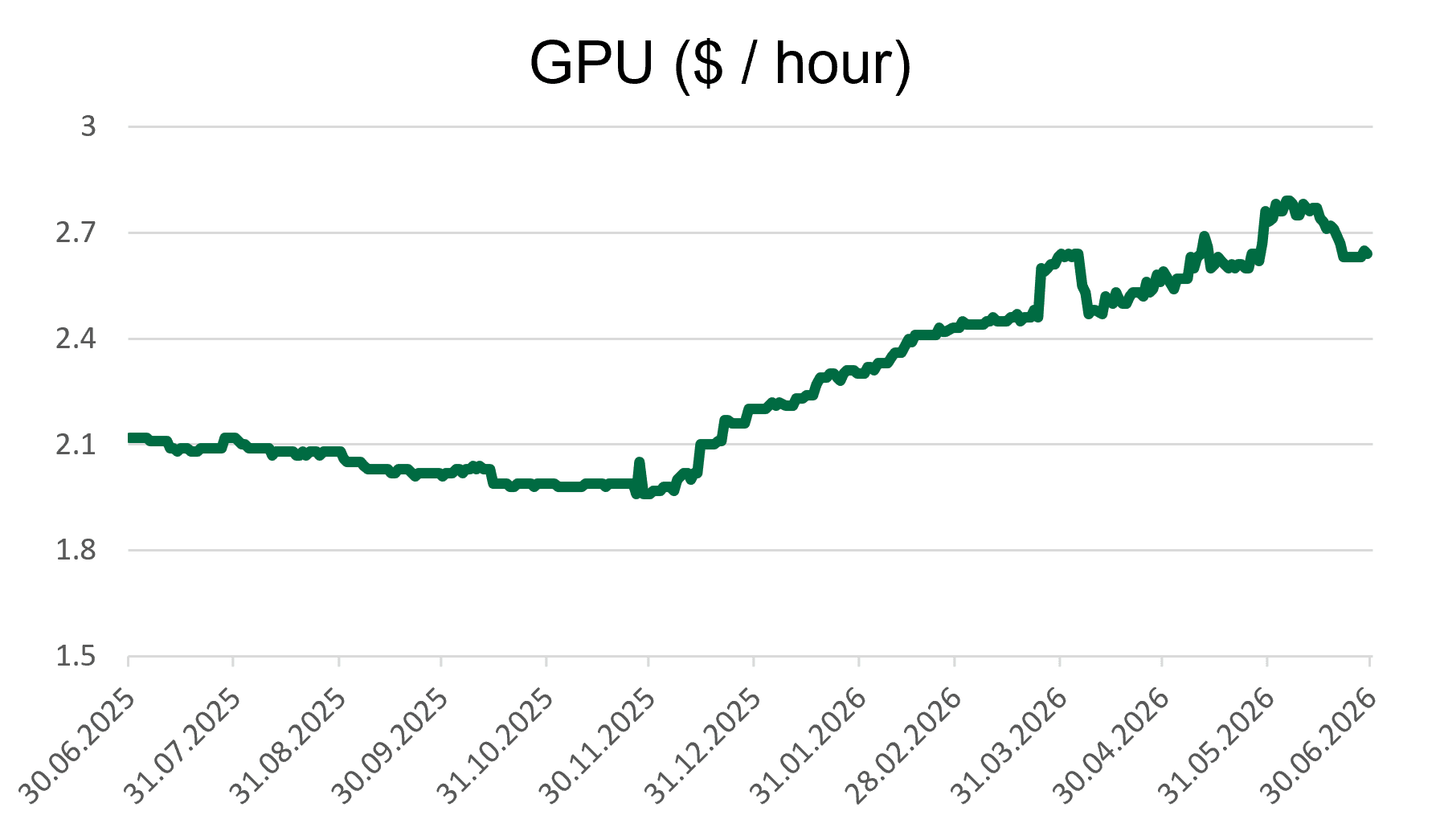

GPU / AI: The cost of AI computing is becoming a new point to watch in commodities. The rental price of H100 GPUs has risen sharply: on one-year contracts, it increased from around USD 1.70 per hour in October 2025 to USD 2.35 per hour in March 2026, an increase of nearly 40%. On the spot market, some indices even stood around USD 7.3 per hour at the end of June, showing that computing capacity remains a rare and expensive asset.

This is an important signal because compute is becoming a key input in the AI value chain. When the hourly price of H100 GPUs rises, it reflects pressure on available capacity in data centers, with strong demand and supply still limited by the availability of chips, electricity and infrastructure.

This market therefore goes beyond semiconductors alone. It directly connects AI, energy and data centers, and may become a leading indicator of tensions in global computing capacity.

This market report was prepared on 06/30/2026.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.