Market Letter - April 2026

Currencies: the energy shock weighs on the euro

EUR/USD: March was marked by strong volatility for the euro, which slipped below 1.17 from the very start of the month. The deterioration in the geopolitical situation in the Middle East and the surge in oil prices weighed heavily on the European currency, pushing it down toward 1.14. Between the February 28 strikes disrupting the Strait of Hormuz and the repeated attacks on transport routes, Brent settled above $100, boosting the dollar’s appeal. The monetary backdrop offered no relief: despite unchanged rates, both the Fed and the ECB struck a more vigilant tone on inflation, putting further pressure on the euro. A brief glimmer of hope emerged at the end of the month after Donald Trump mentioned discussions with Iran, allowing the pair to rebound to 1.16. However, Tehran’s swift denial and the continued deadlock in the conflict pushed the pair back below 1.15 by the close.

EUR/JPY: EUR/JPY remained relatively stable in March, hovering around 183–184. The yen appreciated slightly during periods of market stress, but the move remained limited and was not enough to trigger a sustained decline in the pair. Higher oil prices continued to weigh on Japan, while the BoJ left policy unchanged and core inflation moved back below 2% at month-end. As a result, the yen made only limited gains despite the risk-off backdrop, which restricted the downside in EUR/JPY.

EUR/CHF: The pair fell sharply at the beginning of the month, dropping back below 0.90 during the first strikes in the Middle East and the rise of the Swiss franc as a safe-haven currency. The oil shock, tensions around Hormuz, and the more defensive market environment quickly pushed the euro back to its lowest levels against the franc in more than ten years. The move then reversed. While keeping its policy rate unchanged at 0%, the SNB repeatedly signaled that it was more willing to intervene in the foreign exchange market to curb excessive appreciation of the franc. At the same time, the partial decline in oil prices and Washington’s announcements of a temporary suspension of strikes allowed the pair to recover to 0.917 by the end of the month.

EUR/GBP: The pair declined over the month as a whole, with sterling generally proving more resilient than the euro. The oil shock weighed on both currencies, but the euro area was clearly more heavily penalized due to its greater exposure to rising energy prices. At the same time, the Bank of England left rates unchanged but adopted a firmer tone, which supported sterling and brought the prospect of further hikes back into the debate. The pair, which was trading around 0.877 at the beginning of March, moved back toward the 0.865 area, marking the euro’s worst month against sterling since November 2024.

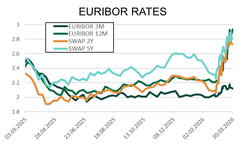

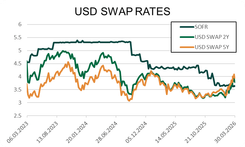

Interest rates: sharp rise in rate expectations as inflation returns

United States: In March, the Fed kept rates unchanged at 3.50–3.75% and maintained in its projections the idea of only one rate cut in 2026. However, the month was marked by a very clear shift in market interpretation. The outbreak of the conflict in the Middle East, the effective closure of Hormuz, and the surge in oil prices quickly brought inflation back to the forefront. Toward the end of the month, Donald Trump’s remarks further amplified the move: his ultimatum on Hormuz, followed by successive announcements about a possible suspension of strikes and discussions with Tehran, triggered sharp swings in rate expectations. In this context, USD yields moved significantly higher across the curve, with the US 10-year rising as high as 4.48%, while the 5-year moved back above 4.14%. The market first priced out the rate cuts that had still been expected before the conflict, and at times even reopened the debate over a possible hike if the energy shock were to persist.

Euro area: Like the other central banks, the ECB left rates unchanged. However, the outbreak of the conflict in the Middle East, the spike in oil prices, and the disruptions around Hormuz brought inflation risk back to the forefront, even as the euro area appears more exposed than the United States to the energy shock. At its March 19 meeting, the ECB raised its 2026 inflation forecast to 2.6% and signaled that it remained ready to act should energy tensions persist. In this context, euro area yields moved significantly higher, especially at the front end of the curve, with the 2-year back at 2.95% and the 5-year around 3.05% by the end of the period. In terms of expectations, whereas the market had still been talking about stability or even cuts before the war, it is now pricing in more than three ECB hikes by December.

Switzerland: From the beginning of the month, the attractiveness of the Swiss franc in the current environment reinforced upward pressure on the currency, prompting the SNB to signal that it was more willing to intervene in the foreign exchange market to curb excessive appreciation of the franc. At its March 19 meeting, it left its policy rate unchanged at 0% and confirmed that stance, acknowledging that the war in the Middle East and the oil shock were altering the monetary environment. At the same time, it slightly raised its 2026 inflation forecast to 0.5%, while reiterating that, at this stage, its main policy lever remained the exchange rate rather than another move on rates. The market is now pricing in two SNB rate hikes in 2026.

United Kingdom: The BoE left its policy rate unchanged at 3.75%, but the oil shock linked to the conflict in the Middle East brought inflation risk back to center stage. At its March 19 meeting, it confirmed a cautious stance, with a unanimous 9–0 vote for the status quo, while also implying that it remained ready to act if tensions in energy prices were to persist. The market therefore significantly raised its rate expectations for the UK, which supported sterling against the euro.

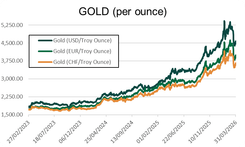

Commodities: hydrocarbon and energy prices surge amid the war in Iran

Oil: The outbreak of the conflict in the Middle East, disruptions around Hormuz, and repeated attacks on regional energy infrastructure quickly pushed Brent above $119/bbl at the height of tensions, before an equally sharp correction following Donald Trump’s announcements of a temporary suspension of strikes targeting Iranian energy sites. The move is still far from stabilized: after falling back to as low as $96/bbl, Brent recovered toward $110/bbl by month-end, while WTI once again fluctuated around $97/bbl. The month was marked by extremely high volatility, with the market entirely driven by developments in the conflict, the risk of lasting supply disruptions, and every public statement capable of shifting sentiment on the duration and impact of the conflict. Oil remains the conflict’s central energy variable in the Middle East, with direct effects across all markets.

Gold: Gold did not play its safe-haven role in a linear way in March. At the beginning of the month, the metal still benefited from the initial shock, before being quickly penalized by the rise in the dollar, oil, and rate expectations. The market is pricing in the inflation risk linked to damage in the energy sector and the rise in central bank policy rates, which removes part of the usual support for precious metals. Gold thus fell back to as low as $4,100/oz this week, its lowest level since November, before rebounding toward $4,400/oz by the end of the period.

Silver: Silver remained under pressure this month. As with gold, the geopolitical backdrop was not enough to provide lasting support for the metal, with the market focusing primarily on rising rates, the dollar, and the inflation shock linked to energy. One ounce of silver was trading around $67 at the end of March.

This market report was prepared on 03/31/2026.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.